Article

SOX vs. SOC Compliance: Key Differences Explained

Eric Sydell, PhD

|

Updated on

|

Created on

When building a compliance program, the first question to ask is: who is this for? The answer is central to the SOX vs SOC compliance decision. The Sarbanes-Oxley Act is for investors, regulators, and the public markets, providing assurance about a company's financial integrity. System and Organization Controls reports are for customers and business partners, offering proof that a service provider can be trusted with their data and operations. While both build trust, they serve different audiences with different needs. Here, we explore these distinctions to help you align your compliance efforts with your most important stakeholders.

Key Takeaways

SOX is a legal rule, while SOC is a customer expectation: The Sarbanes-Oxley Act (SOX) is a federal requirement for public companies focused on financial reporting integrity. System and Organization Controls (SOC) reports are voluntary audits that service organizations use to prove their operational security to clients.

The frameworks address different types of risk: SOX compliance aims to protect investors by preventing financial fraud and ensuring accurate disclosures. SOC reports focus on protecting customer data by validating a service provider's security, availability, and confidentiality controls.

Aligning controls creates efficiency: Organizations that require both SOX and SOC can streamline their efforts by integrating their compliance programs. This approach reduces redundant testing and allows teams to manage evidence for multiple frameworks in a more organized way.

What Is SOX Compliance?

The Sarbanes-Oxley Act of 2002 (SOX) is a federal regulation that establishes auditing and financial standards for all U.S. public companies. Congress passed the act to protect investors by improving the accuracy and reliability of corporate financial disclosures. It was created to prevent accounting fraud and ensure that financial reports are honest.

SOX compliance requires companies to implement and maintain a framework of internal controls. These controls are designed to safeguard financial data and produce accurate reports. The act also created the Public Company Accounting Oversight Board (PCAOB) to oversee the audits of public companies. This oversight helps maintain the integrity of the audit process and holds both companies and auditors accountable.

Core Requirements of the Sarbanes-Oxley Act

The Sarbanes-Oxley Act introduced major changes to the regulation of corporate governance and financial practices. Its core requirements focus on corporate responsibility, enhanced financial disclosures, and fraud accountability. A key mandate is that senior executives, specifically the CEO and CFO, must personally certify the accuracy of their company's financial statements.

This certification makes leadership directly responsible for the information presented to investors. The act also requires companies to establish an independent audit committee to oversee the relationship with the external auditor. These requirements work together to create a system of checks and balances, aiming to restore public trust in corporate accounting and reporting.

Understanding Section 404: Internal Controls

Section 404 is one of the most significant parts of the Sarbanes-Oxley Act. It requires company management to assess and report on the effectiveness of their internal controls over financial reporting. This means companies must document, test, and maintain the processes that ensure their financial data is accurate. An external auditor must also review and issue an opinion on management's assessment.

Achieving SOX compliance is a complex task. It involves a careful mix of people, processes, and technology. Organizations need a strong governance culture and the right expertise to design an internal controls framework that fits the business. This structure helps align compliance efforts with the company's overall strategy and operational realities.

Key Financial Reporting Standards

The ultimate goal of SOX compliance is to ensure transparency and accuracy in financial reporting. Companies achieve this by implementing strong internal controls, which are the rules and procedures that govern how financial data is handled. These controls cover everything from how transactions are recorded to who can access sensitive financial systems.

To verify these controls are working, the Sarbanes-Oxley Act mandates an annual audit by an independent external auditor. This auditor examines the company's financial statements and its internal control structure. The process provides an objective validation that the company's financial reporting is reliable. This independent review is a critical part of the SOX compliance framework.

What Is SOC Compliance?

System and Organization Controls (SOC) compliance is a set of guidelines from the American Institute of Certified Public Accountants (AICPA). These guidelines help evaluate how well a service organization manages its internal controls and processes. Unlike the Sarbanes-Oxley Act, which is a federal requirement for public companies, SOC is a voluntary framework. Service organizations use it to demonstrate their commitment to security and operational integrity to clients.

A SOC report provides customers with assurance that a company has effective systems in place to protect their data. For businesses that rely on third-party vendors for services like data hosting or software-as-a-service, a SOC report is a key part of their risk assessment. It confirms the service provider is managing its operations securely and reliably.

Breaking Down SOC 1, SOC 2, and SOC 3

There are three main types of SOC reports, each serving a different purpose. A SOC 1 report focuses on a service organization's internal controls over financial reporting. This is critical for clients who need to ensure their vendor's processes will not cause errors in their own financial statements.

A SOC 2 report evaluates a company's controls based on five areas known as the Trust Services Criteria. These include Security, Availability, Processing Integrity, Confidentiality, and Privacy. A SOC 3 report covers the same subjects as SOC 2. However, it is a general-use report intended for a public audience and does not include sensitive details about the company’s controls.

What Are the Trust Services Criteria?

The Trust Services Criteria (TSC) are the foundation of a SOC 2 audit. The AICPA established these five categories to provide a framework for evaluating controls over information and systems. The Security criterion is mandatory for all SOC 2 reports and addresses the protection of systems and data against unauthorized access.

The other four criteria are optional. Availability covers the accessibility of systems, Processing Integrity ensures system processing is accurate and timely, Confidentiality protects sensitive information, and Privacy governs the handling of personal information. A service organization selects the criteria that are most relevant to the services it provides to its customers.

Why SOC Matters for Service Organizations

For any service organization, achieving SOC compliance is a clear way to build trust with customers and partners. A successful SOC audit demonstrates that the provider has strong controls in place to protect client data and maintain system availability. This can be a significant competitive advantage, as many companies will not partner with a vendor that cannot provide a SOC report.

Undergoing a SOC audit helps companies strengthen their own security posture by identifying and addressing potential weaknesses. It shows a proactive approach to risk management and a commitment to operational excellence. In today's market, a SOC report is often a non-negotiable requirement for doing business, especially in the technology sector.

Who Needs to Comply with SOX vs. SOC?

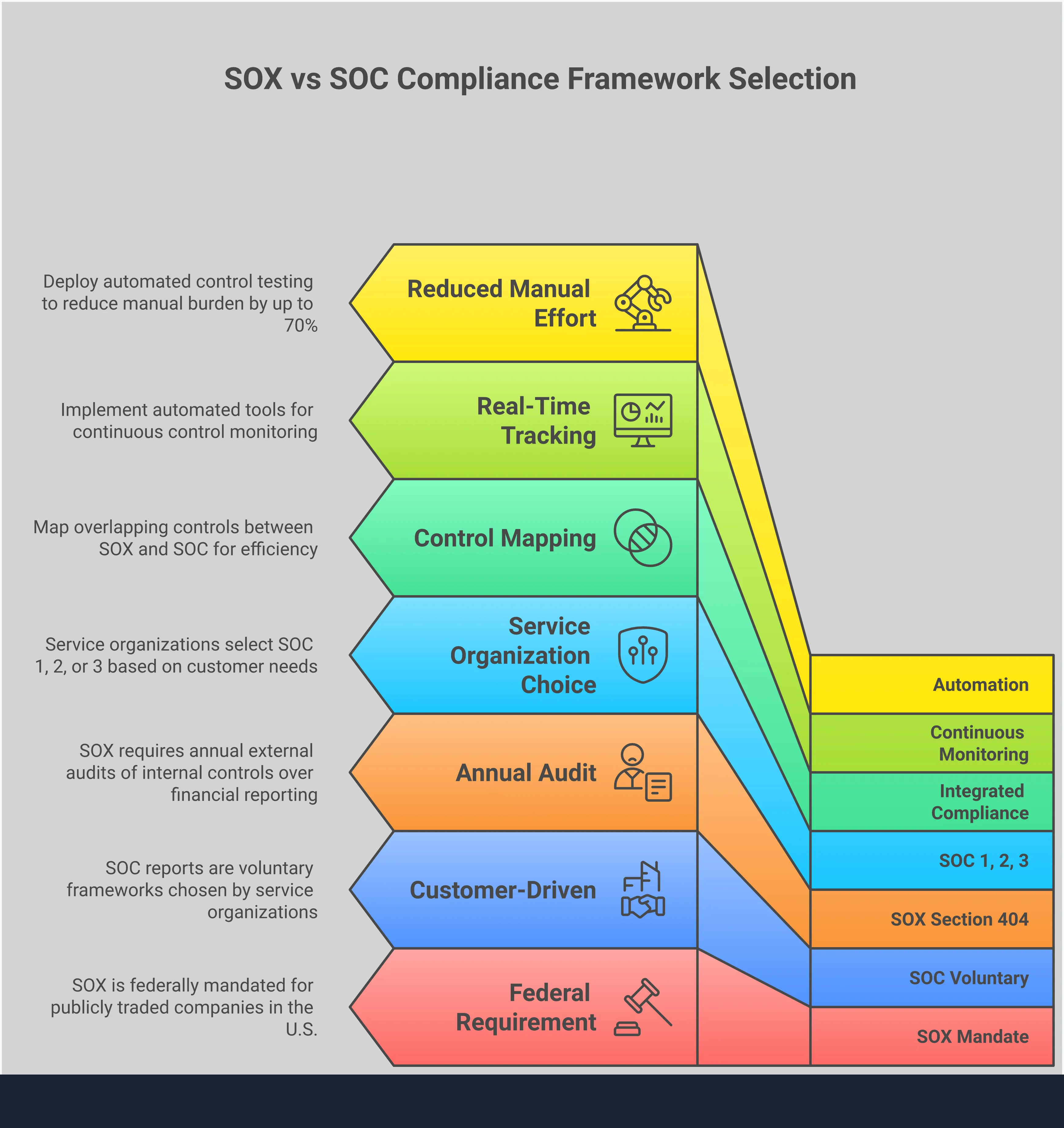

Understanding the distinction between the Sarbanes-Oxley Act (SOX) and System and Organization Controls (SOC) reports starts with one key difference: one is a federal requirement, while the other is a voluntary framework. Your organization’s structure and the services you provide will determine which applies to you. SOX is focused on the accuracy of financial statements for public companies. SOC reports, on the other hand, are designed for service organizations to demonstrate the effectiveness of their internal controls to their customers.

SOX: A Mandate for Public Companies

The Sarbanes-Oxley Act is a US federal requirement that applies to all publicly traded companies. If your company is listed on a public stock exchange in the United States, SOX compliance is not optional. Congress passed the act to protect investors from fraudulent financial reporting by corporations.

To comply, public companies must establish and maintain a system of internal controls over their financial reporting. The effectiveness of these controls must be assessed by management and independently audited by an external firm each year. The goal is to ensure the integrity and accuracy of the financial statements that investors rely on. This makes SOX compliance a critical function for any public company’s finance and audit teams.

SOC: A Voluntary Framework for Service Organizations

System and Organization Controls reports are not required by law. Instead, they are part of a voluntary compliance framework for service organizations. This includes companies that provide services like software as a service (SaaS), cloud computing, or data processing for other businesses. These organizations handle their clients' sensitive data, so they need a way to build trust.

A SOC report provides an independent assessment of a service organization's control environment. While voluntary, SOC compliance often becomes a business necessity. Customers frequently require their vendors to provide a SOC report as part of their due diligence process. It serves as proof that the organization has the proper safeguards in place to protect client data and maintain operational integrity.

SOX vs. SOC: What Are the Key Differences?

While both the Sarbanes-Oxley Act (SOX) and System and Organization Controls (SOC) reports involve audits of internal controls, they serve different purposes. They address distinct risks, apply to different types of organizations, and are driven by different requirements. Understanding these differences is essential for defining your company’s compliance strategy. The main distinctions fall into four categories: their focus, their legal standing, their audit requirements, and their intended audience.

Financial Reporting vs. Operational Controls

The Sarbanes-Oxley Act focuses squarely on a company's internal controls over financial reporting. Its primary goal is to protect investors by ensuring the accuracy and reliability of corporate financial statements. SOX was established to prevent accounting errors and fraudulent practices within public companies.

System and Organization Controls reports, in contrast, evaluate the operational controls at a service organization. A SOC report provides assurance to a company’s clients that their data is handled securely and that the service provider’s systems are reliable. This includes controls related to security, availability, processing integrity, confidentiality, and privacy.

Regulatory Mandate vs. Framework-Based Attestation

Compliance with the Sarbanes-Oxley Act is a legal requirement for all publicly traded companies in the United States. The U.S. Securities and Exchange Commission (SEC) enforces the act, and non-compliance can lead to severe penalties, including fines and imprisonment for executives. SOX is not optional for public companies.

System and Organization Controls compliance, however, is voluntary. It is a framework developed by the American Institute of Certified Public Accountants (AICPA), not a government regulation. Service organizations choose to undergo SOC audits to build trust with their customers. Often, a SOC report becomes a contractual requirement for doing business, as clients need assurance about their vendors' control environments.

Audit Requirements and Frequency

The Sarbanes-Oxley Act requires an annual external audit. An independent auditor must assess and report on the effectiveness of the company's internal controls over financial reporting, as mandated by Section 404 of the act. Management is also required to perform its own assessment and formally assert the effectiveness of these controls.

SOC audits are also performed by independent Certified Public Accountants (CPAs). While not legally mandated, they are typically conducted annually to provide clients with up-to-date assurance. A SOC report covers a specific review period, usually between six and twelve months. This regular cadence helps service organizations demonstrate an ongoing commitment to maintaining a strong control environment for their customers.

Scope and Intended Audience

The scope of the Sarbanes-Oxley Act is specific: it applies to publicly traded companies listed on U.S. stock exchanges and their subsidiaries. The audience for SOX compliance documentation, including audited financial statements, consists of investors, financial analysts, and regulators like the SEC. The goal is to provide transparency for the public capital markets.

The scope for System and Organization Controls is broader, covering any service organization that provides critical services to other businesses. This includes SaaS companies, cloud hosting providers, and payroll processors. The audience for a SOC report is restricted to the service organization's clients and their auditors, who use it to evaluate vendor risk.

How Do SOX and SOC Address Different Risks?

While both SOX and SOC involve audits and internal controls, they are designed to protect against different kinds of business risks. The Sarbanes-Oxley Act targets the integrity of financial information to protect investors. System and Organization Controls reports, on the other hand, focus on the security and operational reliability of service providers to protect customers and their data. Understanding this distinction is key to building the right compliance strategy for your organization.

How SOX Protects Financial Integrity

The Sarbanes-Oxley Act, or SOX, is a United States federal regulation for publicly traded companies. Its primary goal is to prevent corporate fraud and ensure financial reports are accurate and transparent. SOX compliance centers on the internal controls over financial reporting. This means companies must prove they have processes in place to produce reliable financial statements.

The U.S. Securities and Exchange Commission (SEC) enforces these rules. Public companies must undergo regular SOX audits performed by independent external auditors. These audits verify that the company's financial controls are designed effectively and operating as intended, giving investors confidence in the company's reported financial health.

How SOC Strengthens Data Security

System and Organization Controls, or SOC, reports provide assurance about a service organization's systems. These guidelines come from the American Institute of Certified Public Accountants (AICPA). They help companies demonstrate they have the right controls in place to manage customer data securely.

A SOC 2 report, for example, evaluates a company’s controls based on five Trust Services Criteria: security, availability, processing integrity, confidentiality, and privacy. Achieving SOC compliance shows customers and partners that a service provider is committed to protecting their sensitive information and maintaining operational integrity.

What Are the Consequences of Non-Compliance?

Understanding the stakes is critical for any compliance program. While both SOX and SOC frameworks aim to build trust, the consequences of failing to meet their standards are very different. SOX non-compliance can lead to direct legal and financial penalties, whereas SOC gaps primarily result in commercial and reputational damage.

Penalties for Failing a SOX Audit

Failing to comply with the Sarbanes-Oxley Act (SOX) carries significant risks. The consequences of SOX non-compliance can be severe, including large financial penalties and damage to a company's reputation. In some cases, executives can even face criminal charges.

Violating the act can lead to serious legal repercussions. These penalties are designed to hold corporate leadership accountable for the accuracy of financial reports. Even unintentional failures to meet SOX standards can trigger investigations and enforcement actions. Companies that fall short often face a difficult and expensive process to correct their control failures and restore investor confidence.

The Business Cost of SOC Gaps

Unlike SOX, SOC compliance is not a legal requirement. However, failing to maintain it can have a major impact on your business. Many clients now demand SOC reports to ensure their data is safe. A SOC report helps build trust and can give your company an advantage over competitors.

If a service organization cannot provide a SOC report, it may face lost business opportunities. Research from the Ponemon Institute shows that the cost of non-compliance is often much higher than the cost of maintaining a compliance program. These costs include fines, legal fees, and lost business. Ultimately, SOC gaps can disrupt operations and expose a company to significant commercial risk.

Common Challenges in SOX and SOC Implementation

Achieving compliance with the Sarbanes-Oxley Act (SOX) or System and Organization Controls (SOC) frameworks presents significant operational hurdles. While their goals differ, both demand a structured approach to internal controls that can strain internal resources. Many organizations struggle with the volume of work required, from initial implementation to ongoing monitoring and reporting. These challenges often stem from a reliance on manual processes, difficulty integrating controls into existing systems, and the high costs associated with sustained compliance efforts. Overcoming these obstacles requires a clear understanding of where the most common points of friction occur.

The Burden of Manual Testing and Documentation

A major challenge for compliance teams is the heavy reliance on manual evidence gathering and testing. For both SOX and SOC audits, teams must perform thorough testing and documentation of internal controls. This involves chasing down control owners for evidence, reviewing messy PDFs and spreadsheets, and meticulously preparing workpapers. These repetitive tasks consume thousands of hours each audit cycle, diverting skilled auditors from higher-value risk analysis. This manual approach is not only inefficient but also introduces the risk of human error. Such errors can lead to inconsistent testing, documentation gaps, and negative audit findings that erode trust with stakeholders.

Integrating Controls with Existing Systems

Embedding compliance controls into existing business applications and infrastructure is another common difficulty. Many companies run their operations on complex enterprise systems, and ensuring compliance within these environments is not straightforward. For example, organizations often face challenges maintaining segregation of duties (SoD), verifying the accuracy of audit trails, and managing user access controls. When controls are not deeply integrated with the systems they govern, compliance becomes a separate, disconnected activity. This can lead to gaps where automated system processes are not adequately monitored, creating risks that are difficult to detect through manual spot-checks alone.

Managing Change and Training Employees

Compliance is not just about technology and processes; it is also about people. Implementing new controls often requires employees to adopt new workflows and responsibilities. Without effective change management and training, even the best-designed controls can fail. This is especially true in dynamic work environments. As organizations adapt to remote or hybrid work, the need for ongoing training and clear communication becomes even more critical. Every employee who operates a control must understand its purpose and how to execute it correctly. A lack of awareness can lead to unintentional errors and control failures.

The Cost of Implementation and Maintenance

The financial investment required for compliance is a significant consideration for any organization. The average budget for a Sarbanes-Oxley program alone can exceed $1.6 million annually. These costs include external audit fees, salaries for internal compliance staff, and subscriptions for governance, risk, and compliance (GRC) software. The expenses are not a one-time setup cost but a recurring operational burden. While compliance is mandatory for public companies under SOX and a business necessity for many service organizations seeking SOC reports, managing these costs is a key challenge. Organizations must find ways to conduct their compliance programs efficiently to avoid straining their financial resources.

How to Streamline Your Compliance Process

Managing Sarbanes-Oxley (SOX) and System and Organization Controls (SOC) requirements is a significant challenge. These processes often involve repetitive tasks, extensive documentation, and tight deadlines. By adopting modern strategies, you can make your compliance efforts more efficient.

Focusing on automation, continuous monitoring, and integrated governance can transform your compliance program from a burdensome obligation into a strategic asset. These approaches help reduce manual work, provide real-time insights, and create a more cohesive control environment.

Using Automation to Simplify Compliance

Manual compliance testing is often slow and prone to human error. Automation helps solve these problems by handling the repetitive tasks that consume your team’s time. According to research from HubiFi, automated tools can monitor financial data, document controls, and create a clear audit trail.

This ensures that controls are applied consistently every time. By automating routine evidence collection and testing, you can reduce the risk of mistakes and give your team more time for strategic analysis. This shift allows skilled auditors to apply their judgment where it matters most.

Implementing Continuous Controls Monitoring

Traditional audits provide a snapshot of compliance at one point in time. This approach can leave you unaware of control failures that occur between audit cycles. Continuous controls monitoring offers a more proactive solution by evaluating the effectiveness of your controls on an ongoing basis.

This method helps you identify and address issues as they happen, not months later. Implementing continuous monitoring strengthens your internal controls system and helps you adapt to business changes. This approach also helps lower overall SOX costs by reducing last-minute remediation efforts.

Building an Integrated Governance Framework

Many organizations manage SOX and SOC compliance in separate silos, leading to duplicated efforts. An integrated governance framework brings these activities together under a unified strategy. According to analysts at Plante Moran, successful compliance depends on the right combination of people, process, and technology.

By harmonizing your controls across different frameworks, you can reduce redundant testing and gain a clearer view of your organization's risk. This integrated approach also signals a strong commitment to transparency and integrity in your financial operations.

Should Your Organization Use Both SOX and SOC?

The decision between Sarbanes-Oxley Act (SOX) compliance and a System and Organization Controls (SOC) report is not always a choice of one over the other. For many businesses, the two frameworks serve different but complementary purposes. A public company must comply with SOX. If that same company provides services to other businesses, its customers will likely require a SOC report to validate its internal controls.

Pursuing both can be a strategic move. An integrated approach allows an organization to meet its regulatory duties and customer expectations more efficiently. By aligning control testing and evidence collection, teams can reduce redundant work and gain a more complete view of their risk environment. This creates a stronger overall governance structure that satisfies auditors, regulators, and customers.

Finding Overlap Between SOX and SOC Controls

The connection between SOX and SOC is most direct with a SOC 1 report. SOX requires public companies to report on their internal controls over financial reporting. If a company uses a service organization for functions that affect its financial statements, like payroll processing or data center hosting, it often relies on that provider’s SOC 1 report as part of its own SOX assessment.

For a service organization that is also publicly traded, this creates a natural overlap. Many of the financial controls already established to meet Sarbanes-Oxley Act requirements can be used to demonstrate compliance for a SOC 1 audit. This alignment means the organization does not have to build a new set of controls from scratch. Instead, it can leverage existing processes to satisfy both frameworks, saving considerable time and resources.

Developing an Integrated Compliance Strategy

An integrated compliance strategy treats SOX and SOC not as separate projects but as parts of a single governance program. This approach streamlines evidence gathering, since the same evidence can often support controls across both frameworks. It also reduces the burden on control owners and internal audit teams, who can test a control once and apply the results to multiple requirements.

Both SOX and System and Organization Controls compliance require validation from independent external auditors. By aligning the documentation and testing procedures, organizations can make the audit process smoother for everyone involved. A unified strategy helps build trust with investors through reliable financial reporting and with customers through verified operational controls. Using a platform to automate SOX controls can help manage evidence and testing across multiple frameworks in one place.

How to Choose the Right Framework for Your Business

Choosing between SOX and SOC compliance isn't a simple decision. The right path depends on your company's structure, industry, and strategic goals. By carefully considering your specific risks and obligations, you can build a compliance strategy that protects your business and builds trust with stakeholders.

Assess Your Organization's Risk Profile

Your first step is to understand your organization’s unique risks. Compliance challenges often stem from issues with people, processes, and technology. For example, the rise of remote work has introduced new vulnerabilities to internal controls that must be addressed. A comprehensive risk assessment helps you identify where your company is most exposed. By anticipating these challenges, you can determine whether SOX’s focus on financial controls or SOC’s emphasis on operational security is the better fit. This evaluation forms the foundation of an effective and sustainable compliance program.

Evaluate Regulatory Requirements vs. Business Needs

Next, weigh your legal obligations against your business objectives. The Sarbanes-Oxley Act has stringent financial reporting requirements for all publicly traded companies. Non-compliance can lead to severe penalties. For these organizations, SOX is not optional. In contrast, SOC reports are voluntary but often essential for service organizations that handle customer data. Earning a SOC attestation demonstrates a commitment to security and operational integrity, which can be a powerful differentiator. Adopting these compliance best practices helps build confidence among investors, regulators, and customers, turning compliance from a requirement into a strategic asset.

Related Articles

FAQs: SOX vs SOC Compliance

Table of Contents

Eric Sydell, PhD

Eric has two decades of experience in enterprise technology and was a founder of Modern Hire, which became part of Hirevue in 2023.