Article

What is an IIA Audit? A Comprehensive Guide

Eric Sydell, PhD

|

Updated on

|

Created on

Traditional audit methods often struggle to keep pace with the volume and complexity of modern business data. Manual evidence gathering is slow, and annual reviews can miss emerging threats. A strong iia audit program, however, can be adapted for today's environment. By combining the core principles of The Institute of Internal Auditors with modern technology and methods, teams can transform their work. This includes using automation for evidence collection, monitoring risks continuously, and applying agile techniques for faster feedback. This article explains how to strengthen your audit program, moving it from a historical, compliance-focused function to a forward-looking, strategic partner for the business.

Key Takeaways

Understand the foundation of IIA audits: Audits guided by The Institute of Internal Auditors (IIA) are based on global standards for independence and objectivity, designed to provide assurance on risk, governance, and internal controls.

Focus on strategic value beyond compliance: The main purpose of an IIA audit is to help an organization achieve its objectives by assessing risk management, improving governance structures, and analyzing operational efficiency.

Strengthen your audit program with modern practices: Organizations can improve their audit functions by using technology to automate evidence collection, adopting continuous risk monitoring, and applying agile methods for more timely insights.

What is an IIA Audit?

An IIA audit follows a specific set of professional standards designed to help organizations manage risk and improve their operations. These standards are set by The Institute of Internal Auditors (IIA), the profession's global governing body. Understanding the purpose of these audits and the principles behind them is the first step toward building a stronger internal audit function.

Define the IIA Audit and Its Purpose

According to The IIA, internal auditing is an "independent, objective assurance and consulting activity designed to add value and improve an organization’s operations." This means an IIA audit has two main functions. The assurance function provides an objective assessment of your governance, risk management, and control processes. The consulting function advises management on how to improve these processes.

The primary goal is not just to find problems. It is to provide insights that help the organization achieve its objectives. By evaluating how well systems and processes work, internal auditors help leadership make better decisions and operate more effectively. You can read the full definition of internal auditing on the IIA's website.

Explain the Institute of Internal Auditors

The Institute of Internal Auditors (IIA) is the professional organization that sets the standards for the internal audit profession. Founded in 1941, the IIA has grown into a global association that serves members in nearly every country around the world. It acts as the primary advocate, educator, and certifying body for internal auditors.

The organization provides guidance and professional development opportunities to help auditors perform their jobs effectively. This includes offering certifications, conducting research, and publishing guidelines on best practices. The work of The Institute of Internal Auditors ensures that internal audits are conducted with consistency and quality, regardless of the industry or location.

Outline the IIA Code of Ethics

Ethics are central to the internal audit profession. The IIA established its first professional standards in 1978, building on a Code of Ethics created a decade earlier. This code is designed to promote an ethical culture and guide the conduct of internal auditors. It is built on two main components: Principles that are relevant to the profession and Rules of Conduct that describe expected behaviors.

The four core principles are Integrity, Objectivity, Confidentiality, and Competency. Integrity builds trust, while objectivity ensures that auditors remain unbiased in their assessments. Confidentiality requires protecting the information they receive. Competency demands they have the necessary skills and knowledge to perform their duties.

What Standards Guide IIA Audits?

To ensure consistency and quality, internal audits follow a specific set of guidelines. The Institute of Internal Auditors (IIA) provides the globally recognized framework that directs the professional practice of internal auditing. These standards are not just suggestions; they are mandatory requirements for IIA members and Certified Internal Auditors.

The framework establishes principles for how auditors should conduct their work. It covers everything from ethics and independence to planning, execution, and communication. Adhering to these standards helps internal audit functions provide objective assurance and valuable insights to their organizations. They create a benchmark for performance, allowing audit teams to evaluate and improve their own processes. This structure ensures that stakeholders, including management and the board, can trust the audit results.

List the International Standards for Professional Practice

The IIA periodically updates its professional standards to reflect changes in the business and risk environment. The latest version, the Global Internal Audit Standards, became effective in early 2025. This new structure organizes guidance into five main domains, which are supported by 15 guiding principles.

These principles are further broken down into 52 specific standards. Each standard provides clear requirements for auditors to follow. This comprehensive framework guides the daily work of internal auditors and helps them add value to their organizations. It creates a clear roadmap for conducting high-quality audits that meet professional expectations around the world.

Ensure Independence and Objectivity

A core principle of internal auditing is maintaining independence and objectivity. The IIA defines internal auditing as an independent and objective assurance and consulting activity. Independence means the audit function is free from conditions that could compromise its ability to carry out its responsibilities impartially. This is often achieved through the organizational reporting structure, where the chief audit executive reports directly to the board or audit committee.

Objectivity is an unbiased mental attitude that allows auditors to perform their work without compromising quality. It requires auditors to make impartial judgments on all audit matters. This commitment ensures that audit findings are based on evidence and professional analysis, not on influence from management or other parties.

Plan and Execute Audits Effectively

Effective audits begin with careful planning. Auditors following IIA standards invest time at the start of an engagement to understand the environment they are reviewing. This involves identifying key risks and the critical control points designed to manage them. This upfront work ensures the audit focuses on the areas that matter most to the organization.

This risk-based approach allows auditors to tailor their testing procedures to the specific process or technology under review. A well-planned audit is more efficient and produces more relevant findings. It moves beyond simple compliance checking to provide a deeper analysis of how well the organization is managing its most significant risks, a process that can be challenging with traditional methods.

Maintain Quality Assurance

An internal audit function must also monitor its own performance. The IIA standards require every audit department to develop and maintain a Quality Assurance and Improvement Program (QAIP). This program is designed to evaluate the audit function’s conformance with the standards and its overall efficiency and effectiveness.

A QAIP includes both internal and external assessments. Internal assessments involve ongoing monitoring of audit performance and periodic self-reviews. External assessments, or peer reviews, must be conducted at least once every five years by a qualified, independent reviewer. These quality assurance activities help ensure the audit team consistently delivers reliable and high-quality work.

What Are the Main Goals of an IIA Audit?

An internal audit guided by The Institute of Internal Auditors (IIA) standards does more than just check boxes. Its primary purpose is to provide independent assurance that an organization's risk management, governance, and internal control processes are operating effectively. Internal audit functions help an organization accomplish its objectives by bringing a systematic, disciplined approach to evaluating and improving these critical areas.

Instead of focusing only on what went wrong in the past, a modern internal audit looks forward. It helps leadership understand current and emerging risks, identifies opportunities to improve business operations, and provides objective insight to the board and senior management. The main goals of an IIA audit can be broken down into four key areas: managing risk, improving governance, validating controls, and analyzing efficiency. Each goal helps protect and enhance organizational value.

Manage and Assess Risk

A core function of internal audit is to help the organization manage and assess risk. This involves identifying potential threats to the company’s objectives and evaluating how well the business is prepared to handle them. According to guidance on internal audit best practices, the work is designed to "add value and improve an organization’s operations" through a structured approach to risk management. This goes beyond financial risks to include operational, strategic, and compliance-related threats. Auditors provide assurance to leadership that the most significant risks are understood and managed within the company's desired tolerance levels.

Evaluate and Improve Governance

Governance refers to the system of rules, practices, and processes used to direct and control an organization. The internal audit function plays a vital role in evaluating the effectiveness of this system. As The Institute of Internal Auditors states, its mission is to "enhance and protect organizational value by providing risk-based and objective assurance, advice, and insight." Internal auditors assess whether governance structures promote accountability, ethical behavior, and transparency. They review board policies, committee charters, and decision-making processes to ensure they align with the organization's goals and stakeholder expectations.

Test and Validate Internal Controls

Internal controls are the specific actions, policies, and procedures a company uses to mitigate risks and achieve its objectives. A key goal of an internal audit is to test these controls to confirm they are designed correctly and working as intended. This could involve reviewing user access rights for a critical system or verifying that financial transactions are properly authorized. To do this effectively, the IIA requires that "internal auditors must enhance their knowledge, skills, and other competencies through continuing professional development." This ensures they are equipped to evaluate the complex controls found in modern business environments.

Analyze Operational Efficiency

Beyond ensuring compliance and managing risk, internal audits also focus on improving how the business runs. Auditors analyze processes and workflows to identify inefficiencies, waste, and opportunities for improvement. By taking a "systematic, disciplined approach," the internal audit function helps the organization achieve its goals more effectively. This might involve recommending ways to streamline a supply chain, automate a manual reporting process, or reduce operational costs. This focus on efficiency helps position the internal audit team as a strategic partner that contributes directly to the organization's performance and success.

What Challenges Do Organizations Face with IIA Audits?

Internal audit teams must manage a complex landscape of risks and stakeholder expectations. Many departments find it difficult to meet the demands of the organization with their existing resources. These challenges often fall into a few key areas, from staffing and technology to managing time and talent.

Address Resource and Staffing Gaps

Many internal audit departments operate with lean teams. This can create significant pressure to complete audits quickly. According to the Kelmac Group, "Time constraints, staffing shortages, and competing priorities can lead to rushed audits, increasing the risk of overlooking compliance gaps."

When auditors are spread too thin, they may not have enough time for thorough testing or follow-up. This can lead to incomplete assessments and missed opportunities for improvement. The constant pressure to do more with less makes it difficult to provide the deep insights the business needs.

Close Technology and Data Analytics Gaps

Traditional audit methods often struggle to keep pace with the volume and complexity of modern business data. As IT Revolution notes, auditors using a "waterfall audit approach invest time in the beginning of the audit to understand the control environment." This manual, upfront analysis can be slow and inefficient.

Without modern tools, auditors may rely on small sample sizes instead of testing entire populations of data. This approach can miss hidden patterns and outliers. It also makes continuous monitoring nearly impossible, leaving the organization vulnerable to risks that emerge between audit cycles.

Balance Priorities and Time

Determining the right size and focus for an audit team is a significant challenge. As author Richard Chambers explains, factors like company size, industry, and risk profile all play a role. This makes it hard for audit leaders to balance competing priorities and allocate their limited time effectively.

Audit teams must constantly weigh planned audits against special requests from management and the board. They also need to respond to new and emerging risks. For smaller departments, this balancing act is especially difficult, as they have fewer resources to cover a wide range of responsibilities.

Attract and Keep Audit Talent

Finding and retaining skilled auditors is a persistent challenge. The consulting firm Wipfli reports that "attracting and retaining internal audit staff has become a hardship in many sectors." This is partly because the most talented professionals want to focus on strategic work, not repetitive, manual tasks.

When junior auditors spend their days gathering evidence and checking boxes, they can quickly become disengaged. High turnover rates disrupt audit schedules and increase recruiting costs. To keep their best people, audit leaders must find ways to automate routine work and create opportunities for more meaningful analysis.

What Qualifications Do IIA Auditors Need?

Internal auditors need a specific set of qualifications to perform their duties effectively. These qualifications ensure they can provide objective assurance and valuable insights to an organization's leadership. The foundation of these qualifications is a commitment to professional standards, continuous learning, and ethical conduct. Auditors must not only understand the theory behind risk and control but also possess the practical skills to apply that knowledge in complex business environments.

The Institute of Internal Auditors (IIA) sets clear expectations for the professionals who follow its standards. These expectations cover formal certification, ongoing education, and the development of core competencies. Meeting these requirements helps auditors maintain their credibility and ensures the quality of their work. For organizations, having a qualified audit team means receiving reliable assessments that can guide strategic decisions and strengthen governance, risk management, and control processes. A well-qualified auditor is a key asset in protecting and enhancing organizational value.

Earn the Certified Internal Auditor Credential

The most recognized qualification in the field is the Certified Internal Auditor (CIA). According to The Institute of Internal Auditors, the Certified Internal Auditor (CIA) is the only globally accepted certification for the profession. Earning this credential demonstrates that an auditor has the knowledge and skills to conduct internal audits in accordance with international standards.

The CIA exam covers key areas of the internal audit practice, including governance, risk management, and control. Holding this certification signals a deep commitment to the profession and to upholding a high standard of practice. It shows that an auditor is not just familiar with the principles of internal auditing but has proven their expertise in a formal, globally recognized assessment.

Meet Continuing Education Requirements

The work of an internal auditor is never static. Risks evolve, regulations change, and new technologies emerge. Because of this, continuing education is not just recommended; it is a requirement. The IIA’s standards state that "internal auditors must enhance their knowledge, skills, and other competencies through continuing professional development."

This requirement ensures that auditors stay current on the latest trends and techniques in their field. It involves participating in training, attending conferences, and pursuing other educational opportunities. By continuously learning, auditors can provide more relevant and effective assurance and advice. This commitment to lifelong learning is essential for maintaining professional competence and delivering high-quality audit services.

Build Core Skills and Competencies

Beyond formal certifications and education credits, effective auditors must develop a range of core skills. These include critical thinking, communication, data analytics, and a thorough understanding of business operations. These competencies are what allow an auditor to translate technical knowledge into actionable insights for the organization.

As one Internal Auditor Magazine article notes, professional development is "integral to ensuring auditor competency and a requirement for maintaining the effectiveness and quality of internal audit services." Strong analytical skills help auditors identify the root cause of a problem, while clear communication skills are needed to explain complex issues to stakeholders. Building these competencies is a continuous process that separates a good auditor from a great one.

Pursue Ongoing Professional Development

The mandate for professional development is formally embedded within the standards that govern the profession. The Global Internal Audit Standards explicitly require ongoing development to improve the quality and effectiveness of audit work. This goes beyond simply earning credits; it is about a proactive approach to skill enhancement.

This means auditors should actively seek opportunities to grow. This could involve specializing in a high-risk area like cybersecurity, learning new data analysis tools, or taking courses on leadership and communication. Pursuing professional development shows a dedication to excellence and helps ensure that the internal audit function remains a valuable partner to the business, capable of addressing both current and future challenges.

How Can Organizations Strengthen IIA Audit Programs?

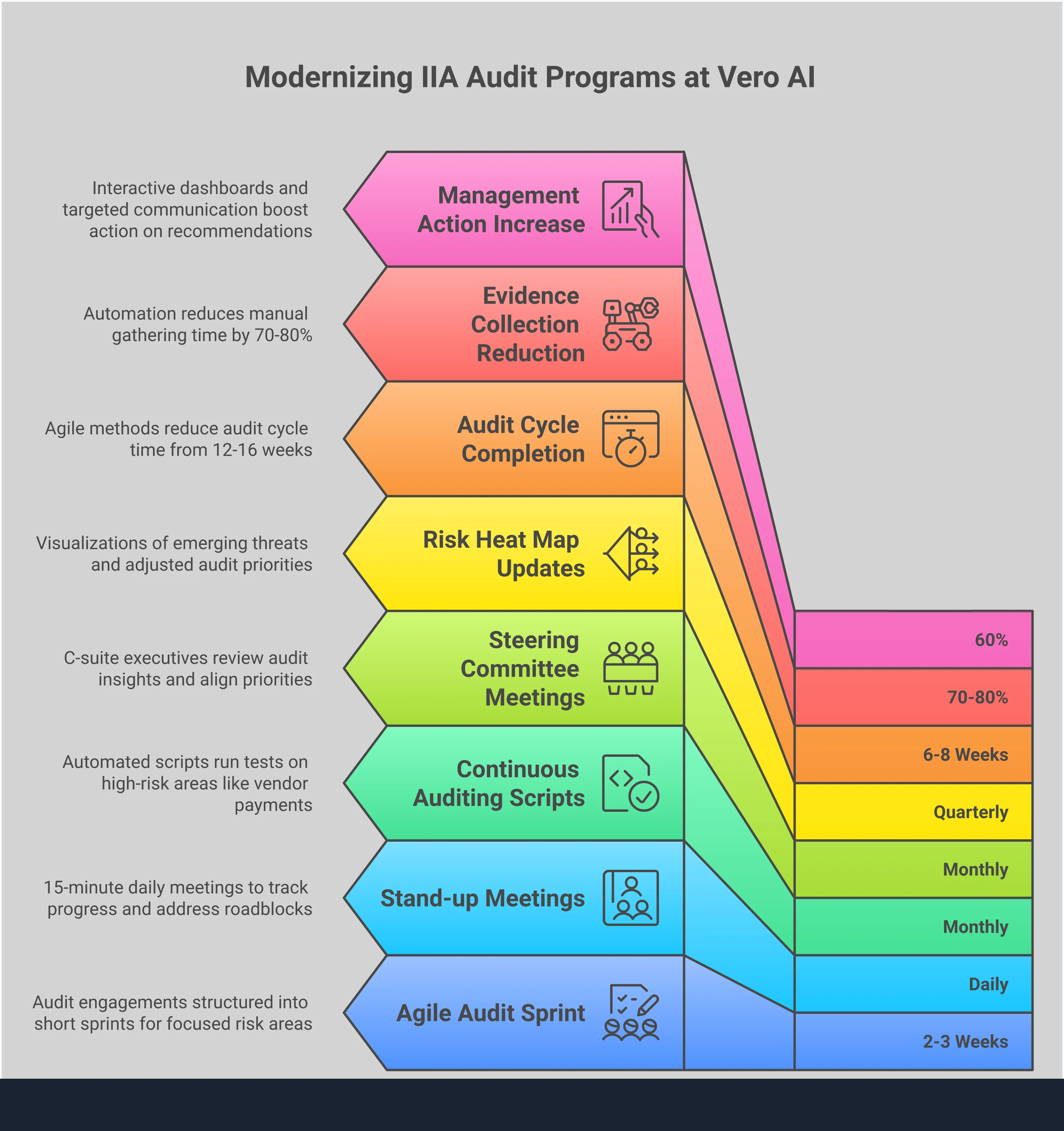

A strong internal audit program does more than check boxes for compliance. It provides strategic insight and helps the organization manage risk effectively. To meet the demands of a complex business environment, audit teams are adopting new methods. These include using technology for better evidence collection, monitoring risks continuously, applying agile techniques, and improving communication with stakeholders. These practices help transform the audit function from a cost center into a strategic partner.

Use Technology for Evidence Collection

Traditional audits rely on manual evidence gathering, which is slow and can introduce errors. Modern audit teams use technology to automate this work. According to a report from Plante Moran, "AI-powered tools enable internal auditors to expand the scope of their audits, assessing more risk factors, resulting in audits that are more thorough, with fewer blind spots and enhanced compliance." Automation platforms can connect to different systems, pull relevant documents, and organize them for review. This frees auditors from repetitive tasks. They can spend more time on analysis, judgment, and advising the business on important risks.

Monitor Risks Continuously

Risks change quickly, and annual audits can miss emerging threats. Continuous monitoring helps teams stay ahead. This approach involves using technology to track controls and key risk indicators in near real-time. An Enterprise Risk Management (ERM) program provides a framework for this proactive stance. Instead of discovering a control failure months after it happened, continuous monitoring systems can flag issues immediately. This allows the organization to respond faster and reduce potential damage. It shifts the audit function from a historical reviewer to a forward-looking advisor.

Apply Agile Audit Methods

The traditional audit process can be long, with findings delivered months after fieldwork begins. Agile auditing offers a more flexible alternative. This method uses short, focused cycles called sprints to assess risks and test controls. Teams collaborate closely with business stakeholders and provide frequent updates. This approach was adopted by companies like Capital One, which "experienced challenges with the traditional audit approach, both from the auditor’s perspective and across the rest of the organization," according to the Institute of Internal Auditors. Agile methods help ensure that audit findings are timely, relevant, and aligned with the organization's current priorities.

Build Strong Stakeholder Communication

An audit’s value depends on how well its findings are communicated and understood. Building strong relationships with stakeholders is essential. Technology can help by providing clear, data-driven insights. Instead of static reports, auditors can use dashboards to show risk trends and control performance. As experts at Plante Moran note, audit teams can "engage internal stakeholders with AI insights: Use AI-driven analysis to align audit goals, risks, and compliance requirements, ensuring informed agreement on key priorities." This collaborative approach builds trust and helps ensure that audit recommendations lead to meaningful improvements across the business.

Related Articles

IIA Audit FAQs

Table of Contents

Eric Sydell, PhD

Eric has two decades of experience in enterprise technology and was a founder of Modern Hire, which became part of Hirevue in 2023.