Article

What Is an Internal Auditor? A Complete Guide

Mike Reeves, PhD

|

Updated on

|

Created on

Business operations are increasingly driven by data and technology. This shift has fundamentally changed the work of an internal auditor. The role is no longer limited to reviewing historical records in small samples. Today, auditors use data analytics tools to examine entire populations of data, identifying anomalies and emerging risks in real time. They must also possess expertise in areas like cybersecurity and automated systems to evaluate the controls that protect an organization's most critical assets. This technical skill set allows the modern internal auditor to provide forward-looking insights, helping the organization prepare for future challenges in a complex and fast-changing environment.

Key Takeaways

Internal auditors are strategic partners: They provide independent evaluations of a company's risk management, controls, and compliance processes to help the organization operate more efficiently and protect its value.

The audit process requires modern skills: A successful audit follows a clear cycle of planning, testing, and reporting, and relies on skills in data analytics and stakeholder communication to be effective.

Internal audit strengthens governance: By reporting directly to the board's audit committee, auditors provide unbiased assurance that strengthens oversight, supports risk management, and helps maintain ongoing compliance.

What Is an Internal Auditor?

An internal auditor is a professional who provides an independent and objective evaluation of a company's operations. They examine the effectiveness of an organization's risk management, internal controls, and governance processes. Their primary goal is to help the organization operate more efficiently and achieve its objectives.

Internal auditors act as trusted advisors to management and the board of directors. They provide insights and recommendations based on their analyses and assessments of data and business processes. By identifying areas for improvement, they help protect the organization's assets and reputation while ensuring compliance with regulations. This function is critical for maintaining organizational health and building a resilient business.

Defining the Role and Its Purpose

Internal auditors are objective assurance professionals. They are employed by an organization to add value and improve its operations. Their main job is to ensure the company follows rules, manages risks effectively, and meets its strategic goals. They provide independent advice and insights to the company's leadership.

The scope of internal audit is broad. It covers everything from the reliability of financial reporting to the efficiency of operations and compliance with regulations. According to the Institute of Internal Auditors (IIA), this work helps an organization accomplish its objectives by bringing a systematic, disciplined approach to evaluate and improve the effectiveness of risk management, control, and governance processes.

Internal vs. External Auditors

The roles of internal and external auditors are distinct. Internal auditors are employees of the company. They conduct ongoing audits throughout the year and report their findings directly to management and the audit committee. Their focus is broad, covering financial, operational, and compliance risks to help the business improve.

External auditors, on the other hand, are independent contractors hired by a company. Their primary responsibility is to express an opinion on the fairness of the company's financial statements. They perform a single annual audit and report to shareholders and other external parties. While both roles require objectivity, their audiences and objectives are fundamentally different.

Debunking Common Myths

A common myth is that internal auditors exist only to find mistakes and assign blame. This perception can create a negative culture around the audit process. In reality, the role is constructive. Internal auditors are partners who help identify problems and find solutions from within the organization.

Another misconception is that auditing is a stagnant career. Internal auditing offers significant opportunities for professional growth. Auditors gain a deep understanding of the entire business, which prepares them for leadership roles. They play a key part in a company’s success by proactively identifying and addressing issues, making them essential to long-term organizational health.

What Are an Internal Auditor's Key Responsibilities?

An internal auditor acts as an organization's independent advisor. Their work focuses on improving operations and ensuring financial reliability and compliance. They provide objective analysis and recommendations to management and the board of directors. This helps the organization achieve its objectives by bringing a systematic, disciplined approach to evaluating and improving the effectiveness of risk management, control, and governance processes.

The responsibilities of an internal auditor are broad. They are not just focused on financial numbers. They examine the efficiency of operations, the reliability of financial reporting, and the company's compliance with regulations and internal procedures. By identifying weaknesses and suggesting improvements, they play a critical role in maintaining the organization's health and integrity. Their work is divided into four main areas: assessing risk, testing controls, monitoring compliance, and communicating their findings to leadership. Each area is essential for providing a complete picture of the organization's performance and risk exposure.

Assessing and Managing Risk

A primary responsibility for internal auditors is to identify and assess risks. They examine company records and processes to find potential threats to the organization's success. This includes financial risks, operational inefficiencies, and strategic challenges. Auditors help the company understand its risk landscape.

By looking for potential problems, auditors allow the organization to be proactive. They analyze how different departments operate and communicate to find areas of vulnerability. This process of risk assessment helps leadership make informed decisions to protect the company's assets and reputation. Their goal is to help the company manage uncertainty and turn potential threats into manageable challenges.

Evaluating and Testing Controls

Internal auditors evaluate the internal controls that a company puts in place. Internal controls are the processes and procedures designed to manage risks and help the company achieve its goals. Auditors test these controls to make sure they are working correctly and effectively.

This involves reviewing financial reports, observing operational processes, and analyzing data. According to the professional education resource Becker, auditors look for inefficiencies or instances of non-compliance to help fix them quickly. By testing controls, they provide assurance to management that the systems in place are reliable and capable of preventing errors or fraud.

Monitoring Compliance

Ensuring the company follows all relevant rules is another key duty. Internal auditors are responsible for verifying that the organization adheres to external regulations and its own internal policies. This is a critical function for avoiding legal penalties and maintaining public trust.

Auditors check for compliance with a wide range of requirements. This can include information security standards like ISO 27001 or healthcare data protection regulations like the Health Insurance Portability and Accountability Act (HIPAA). They review documents, interview staff, and test systems to confirm that the company meets its obligations. This oversight helps protect the organization from costly fines and reputational damage.

Communicating Findings

After completing their assessments, internal auditors must clearly communicate their findings. This is perhaps their most important function, as effective reporting is what drives action and improvement. They prepare detailed reports for senior management and the board of directors.

These reports outline identified risks, control weaknesses, and compliance gaps. According to The Institute of Internal Auditors (IIA), Chief Audit Executives (CAEs) must present their plans and findings to leadership for review. The reports also include practical recommendations for fixing the problems. Clear and credible communication of results ensures that decision-makers understand the issues and can take the necessary steps to strengthen the organization.

How Do You Become an Internal Auditor?

A career in internal audit is built on a foundation of formal education, professional credentials, and specific personal competencies. The path is structured, requiring a commitment to learning and high ethical standards. Aspiring auditors can follow a clear progression to enter and advance in the field, starting with a relevant degree and continuing with specialized certifications and skill development. Each step prepares you to handle the complexities of assessing risk, controls, and governance within an organization.

Educational Background

Most organizations require internal auditors to have at least a bachelor's degree. Common fields of study include accounting, finance, or business administration. These programs provide a strong understanding of financial principles, business operations, and regulatory environments. According to career resource Indeed, some employers prefer candidates with a master's degree in accounting or an MBA with an accounting focus, especially for roles that require specialized knowledge or offer a faster track to leadership. This advanced education can provide deeper expertise in complex audit areas and strategic business functions.

Professional Certifications

While a degree is essential, professional certifications demonstrate a higher level of expertise and commitment to the profession. The most recognized credential is the Certified Internal Auditor (CIA), offered by The Institute of Internal Auditors (IIA). Earning the CIA designation validates your knowledge of internal audit best practices, risk management, and governance. The IIA provides resources like the CIA Learning System to help candidates prepare for the rigorous exam. Holding this certification often leads to greater career opportunities and is a common requirement for senior and management-level positions in the audit field.

Essential Skills and Competencies

Successful internal auditors combine technical knowledge with strong soft skills. Core competencies include a deep sense of professionalism, ethics, and fairness. Strong analytical skills are critical for evaluating evidence, identifying risks, and understanding complex business processes. Auditors must also be excellent communicators, capable of clearly explaining their findings and recommendations to management and stakeholders. Integrity is non-negotiable, as auditors must remain objective and independent. The ability to continuously learn is also vital for keeping up with changing business environments, technologies, and regulations.

How Does the Internal Audit Process Work?

The internal audit process follows a structured, cyclical approach to provide objective assurance to an organization's leadership. While the specifics can vary based on the company and industry, the core process generally includes four distinct phases. Each phase builds on the last, from initial planning and risk assessment to long-term monitoring. This systematic method ensures that audits are thorough, consistent, and valuable for improving business operations and governance. Understanding these steps helps clarify how internal auditors contribute to an organization's health and integrity.

Planning and Scoping the Audit

The internal audit process begins with careful planning. In this initial phase, auditors define the scope of the audit, outlining exactly which departments, processes, or systems will be reviewed. A key part of this stage is to assess the risks associated with the area under review. This involves identifying potential vulnerabilities, control weaknesses, or compliance gaps that could impact the organization. This foundational step is critical because it sets the objectives and direction for the entire audit, ensuring that the team focuses its efforts on the areas that matter most to the business.

Conducting Fieldwork and Testing

Once the plan is set, auditors move into the fieldwork phase. This is where the team actively gathers evidence to evaluate the effectiveness of internal controls and processes. Auditors use several techniques, including interviewing employees, observing operations, and performing detailed data analysis. The goal is to collect sufficient, reliable information to form an objective opinion. This hands-on work is essential for understanding how processes function in practice, not just on paper. It allows auditors to test the controls in place and verify whether they are working as intended.

Reporting Key Findings

After completing the fieldwork, auditors analyze their findings and compile them into a formal audit report. This document is a key deliverable of the internal audit function. It summarizes the audit's scope, objectives, and overall conclusions. The report highlights significant issues, control deficiencies, and areas of non-compliance identified during the review. Crucially, it also provides actionable recommendations for improvements to address the identified weaknesses. This report is typically shared with senior management and the audit committee of the board of directors, providing them with clear insights into the organization's operations.

Following Up and Monitoring Progress

The audit process does not end when the report is delivered. The final step is follow-up, where auditors track the implementation of their recommendations. This involves verifying that management has taken the agreed-upon corrective actions to address the findings from the audit report. This monitoring is vital for ensuring accountability and driving real improvement within the organization. By following up on progress, internal audit helps close the loop on identified issues and reinforces a culture of continuous improvement and strong governance across the business.

What Are the Main Types of Internal Audits?

Internal audit functions cover a wide range of activities to address an organization's diverse risks. Instead of a single, uniform approach, auditors conduct several types of audits, each designed to evaluate a specific area of the business. These assessments help leadership understand whether operations are efficient, financial reports are accurate, and the company is following all relevant rules.

The scope of an internal audit depends on the organization's objectives, industry, and risk profile. A manufacturing company might prioritize operational audits of its supply chain, while a financial services firm may focus more on compliance and IT security. By tailoring their approach, internal auditors provide targeted insights that help the organization manage risk and improve performance. The main categories of internal audits include financial, operational, compliance, and information technology (IT) audits. Each type serves a distinct purpose in the overall governance and control structure.

Financial Audits

Financial audits are one of the most traditional forms of auditing. Their primary goal is to confirm the integrity and accuracy of an organization's financial records. According to Sacramento State, financial audits review financial records and reporting accuracy, ensuring that the financial statements are free from material misstatement and comply with applicable accounting standards.

Auditors examine transactions, test internal controls over financial reporting, and verify account balances. This process helps detect errors or potential fraud. By providing an independent assessment of financial statements, these audits give the board, management, and other stakeholders confidence in the company's reported financial position and performance.

Operational Audits

Operational audits look beyond the numbers to evaluate how a business runs. These audits focus on the efficiency and effectiveness of an organization's processes. As defined by Sacramento State, operational audits examine the effectiveness and efficiency of an organization's operations, focusing on the processes and procedures in place to achieve business objectives.

An auditor might review a company's procurement process to identify bottlenecks or evaluate a customer service department's workflow to find opportunities for improvement. The findings from an operational audit often lead to recommendations for streamlining activities, reducing costs, and better aligning daily operations with strategic goals.

Compliance Audits

Compliance audits determine whether an organization is following applicable regulations, standards, and its own internal procedures. This type of audit is critical for managing legal and regulatory risk. Sacramento State explains that compliance audits verify that an organization adheres to regulatory requirements, legal standards, and internal policies, ensuring that operations are conducted within the established guidelines.

For example, an auditor might check if a healthcare provider complies with the Health Insurance Portability and Accountability Act (HIPAA) or if a company meets the requirements of the ISO 27001 standard for information security. These audits help organizations avoid fines, penalties, and reputational damage associated with non-compliance.

IT and Cybersecurity Audits

In an increasingly digital world, IT and cybersecurity audits are essential. These audits evaluate the controls that protect an organization's information systems and data. The focus is on safeguarding confidentiality, integrity, and availability. Sacramento State notes that IT and cybersecurity audits assess the effectiveness of an organization's information technology controls, focusing on data security, system integrity, and the overall management of IT resources.

Auditors may review everything from network security and access controls to data backup and disaster recovery plans. These assessments identify vulnerabilities that could lead to data breaches or system failures, helping the organization strengthen its defenses against cyber threats.

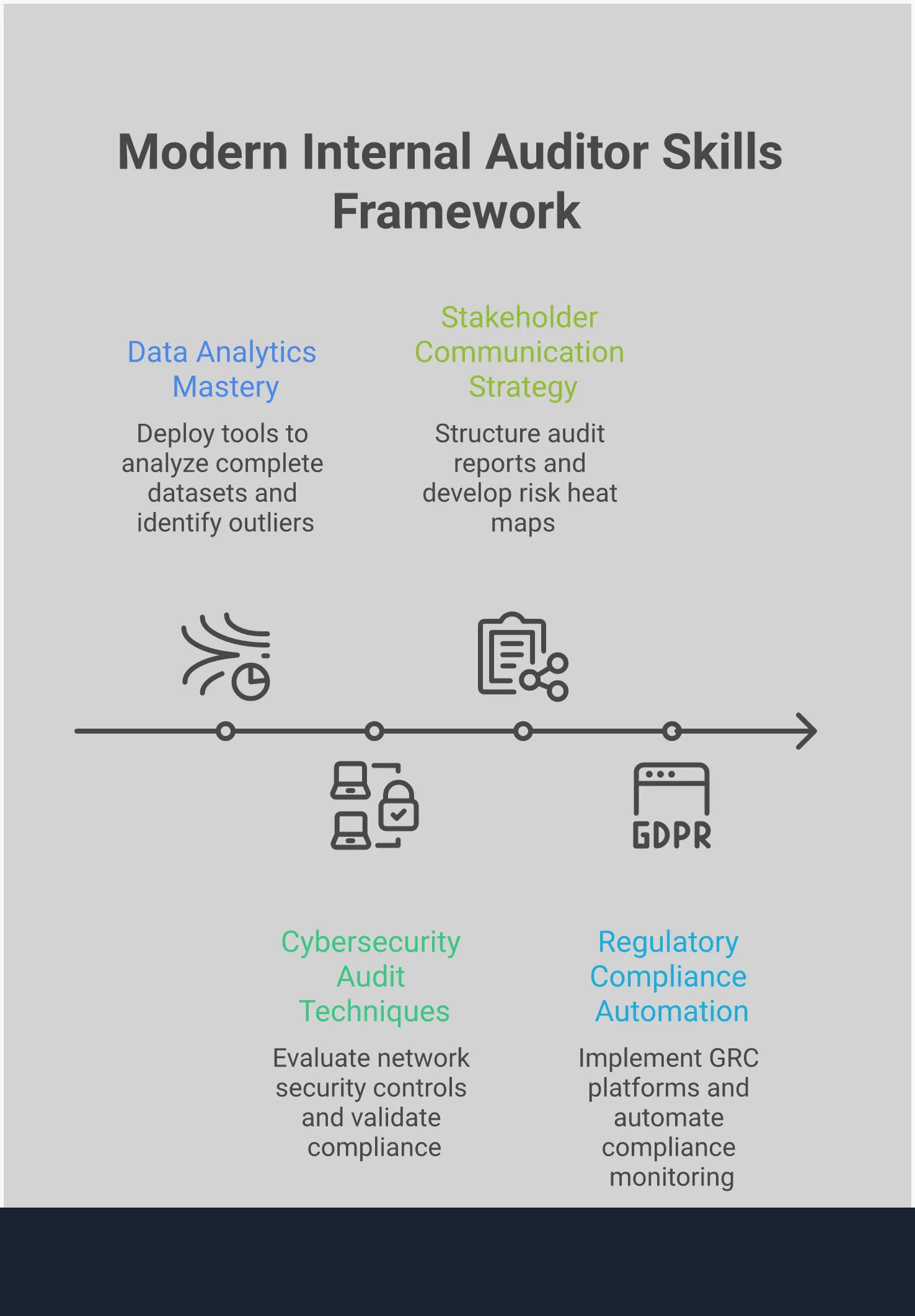

What Skills Does a Modern Internal Auditor Need?

The role of an internal auditor has expanded far beyond traditional financial checks. Today’s business environment is shaped by complex regulations, digital transformation, and evolving risks. To be effective, auditors need a modern skill set that combines technical knowledge with strong interpersonal abilities. They must act as trusted advisors who can analyze complex data, communicate clearly with leadership, and continuously adapt to change. This blend of skills allows them to provide valuable insights that help organizations manage risk and achieve their objectives.

Data Analytics and Technology

Internal auditors now work with massive volumes of data. Instead of relying on small samples, they can use technology to analyze entire datasets, identify anomalies, and spot emerging risks. A strong grasp of data analytics tools is no longer optional; it’s essential for conducting efficient and thorough audits. Using audit management software helps improve the quality and speed of audit processes. This technical skill allows auditors to move from simply reviewing past events to providing forward-looking insights that help the business prepare for future challenges.

Stakeholder Communication

An audit’s findings are only useful if they are understood and acted upon. Modern auditors must be excellent communicators who can translate complex information into clear, credible reports for management and the board. According to The Institute of Internal Auditors (IIA), effective reporting is where internal audit creates its impact. The Chief Audit Executive (CAE) is responsible for communicating the internal audit activity’s plans and resource requirements to senior leaders. This requires tailoring the message to different audiences, from technical teams to board members, ensuring everyone understands the risks and recommended actions.

Continuous Learning and Regulatory Expertise

The landscape of risk and regulation is always changing. Auditors must be committed to continuous learning to keep their knowledge current. As new technologies reshape business operations, audit teams must expand their capabilities to match. This involves staying informed about emerging cybersecurity threats, new privacy regulations, and changes to industry standards. To perform their duties effectively, auditors need the technical expertise to evaluate how new technologies impact internal controls and financial reporting. This dedication to learning ensures they remain a valuable resource for their organization.

What Does a Career Path in Internal Audit Look Like?

A career in internal audit offers a clear path for advancement. Professionals can grow from entry-level positions to executive leadership roles. The journey involves developing technical skills, business acumen, and strong communication abilities. This path allows auditors to gain a deep understanding of an organization's operations, risks, and strategic goals.

Entry-Level and Progression

Most internal audit careers begin with a role like staff auditor or internal audit assistant. In these positions, you learn the fundamentals of the audit process. You will execute test plans, document evidence, and help identify control weaknesses. This hands-on experience builds a strong foundation for future growth.

As Becker explains, "Internal auditors can start in entry-level jobs like an internal audit assistant and move up to senior roles like audit manager, internal audit director, or even CFO." After a few years, a staff auditor can advance to a senior auditor position. Senior auditors take on more complex audit areas, guide junior staff, and begin to interact with business process owners.

Senior Roles and Specializations

With more experience, auditors can move into management. An audit manager or senior manager oversees entire audit projects from planning to reporting. They manage teams of auditors and are responsible for the quality of the audit work. These roles require strong project management and leadership skills.

According to Accounting.com, "Experienced internal auditors can move up to senior roles, where they oversee audits and talk to top management about risks." This increased interaction with leadership is a key part of the role. Auditors at this level may also choose to specialize in high-demand areas like information technology audits, fraud investigations, or environmental compliance.

Management and Executive Tracks

The top position in the field is the Chief Audit Executive (CAE). The CAE is a senior leader who sets the direction for the entire internal audit function. They develop the annual audit plan, manage the department's budget, and provide strategic advice to the executive team and the board of directors.

The Institute of Internal Auditors states, "The CAE must report to a level within the organization that allows the internal audit activity to fulfill its responsibilities," often meaning a direct line to the audit committee. To reach this level, auditors must demonstrate a deep understanding of the business. As MetricStream explains, successful auditors are those who can "keep pace with the risks and changes in the business environment" and "deliver timely and forward-looking insights."

How Do Internal Auditors Overcome Common Challenges?

The work of an internal auditor involves more than reviewing documents and testing controls. Auditors often face complex situations that test their skills and judgment. Successfully handling these challenges is key to providing value to their organizations. Key areas include maintaining impartiality, keeping up with new rules, and communicating effectively with leadership.

Maintaining Independence and Objectivity

To provide a fair assessment, internal auditors must remain independent from the operations they review. This allows them to identify issues without internal pressure or bias. As noted in a resource from Accounting.com, auditors need to act independently to find problems fairly. This separation is often built into the company’s structure. The internal audit function typically reports directly to the audit committee of the board of directors, not to the management teams they are auditing. This reporting line helps protect the audit team’s ability to deliver objective insights and maintain professional integrity.

Adapting to Evolving Regulations

Business and regulatory environments are always changing. Internal auditors must continuously update their knowledge to remain effective. According to ISACA, the profession faces new challenges related to global business, expectations for environmental, social, and governance (ESG) factors, and new technology. To keep pace, auditors invest in ongoing education and professional development. They also use technology to monitor regulatory changes and adapt their audit plans to address new risks, ensuring the organization remains compliant.

Managing Stakeholder Communication

An audit’s findings are only useful if they are understood and acted upon. This makes communication a critical skill for internal auditors. The Institute of Internal Auditors (IIA) states that clear and credible reporting is where the function creates its impact. Auditors must present their findings clearly to different audiences, from operational managers to the board. The Chief Audit Executive (CAE) is also responsible for communicating the audit team’s plans and needs to senior management. This proactive communication ensures everyone is aligned and that the audit function has the resources it needs.

How Can Internal Auditors Communicate Findings Effectively?

An internal audit adds little value if its findings are not understood or acted upon. Effective communication is the bridge between identifying a risk and fixing it. It transforms your audit report from a simple document into a catalyst for positive change. To ensure your work has a real impact, you need a clear strategy for sharing what you’ve found with the right people, in the right way. This involves creating clear reports, tailoring your message to the audience, and following up on your recommendations.

Adopt Clear Reporting Strategies

Your audit report is the primary vehicle for your findings, so it must be direct and easy to digest. According to The Institute of Internal Auditors (IIA), "Clear, credible reporting is where internal audit creates impact." To achieve this, avoid technical jargon and focus on a simple structure for each finding. Describe the condition (what you found), the criteria (what it should be), the cause (why it happened), and the consequence (the risk to the business). This approach helps stakeholders quickly grasp the issue. Your goal is to present information in a way that enables management to make confident and timely decisions based on your audit reporting.

Tailor Communication for Different Audiences

Not everyone needs the same level of detail. The board of directors requires a high-level summary of significant risks, while a department manager needs specific, actionable steps to address a control weakness. As The IIA notes, the Chief Audit Executive (CAE) must communicate plans and resource requirements to senior management and the board for review. This highlights the need for tailored communication. An effective auditor adjusts the message, format, and depth of information for each audience. This ensures your findings are relevant and resonate with each stakeholder group, prompting the right conversations and actions at every level of the organization.

Track Recommendations and Follow-Up

The audit process does not end when you issue the report. Ensuring that management acts on your findings is a critical final step. An effective follow-up process is crucial for confirming that management has implemented the agreed-upon actions to mitigate risks. This involves establishing clear timelines, assigning ownership for each recommendation, and periodically checking on progress until the issue is resolved. This systematic tracking holds the organization accountable and demonstrates the value of the internal audit function. It closes the loop, confirming that identified weaknesses have been strengthened and the organization is more resilient as a result of your work.

How Do Internal Auditors Support Governance?

Internal auditors are a key part of an organization's governance framework. Governance is the system of rules, practices, and processes used to direct and control a company. It provides the structure for achieving objectives while balancing the interests of stakeholders like management, customers, and regulators. Internal audit strengthens this structure by providing independent assurance.

Auditors evaluate how well the organization manages its risks. They also check if its internal controls are working effectively. They act as a critical check and balance, helping ensure the company operates ethically and complies with relevant regulations. This function is not just about finding problems; it is about offering insights to improve processes and strengthen the overall control environment.

A strong internal audit function supports governance in several ways. It establishes clear communication with the board of directors, integrates its work with risk management, and helps the organization maintain a constant state of audit readiness. These activities provide leadership with confidence that the organization is on the right track.

Reporting to the Board and Audit Committee

An internal auditor's effectiveness depends on independence. To achieve this, the internal audit function must have a direct reporting line to the board of directors and its audit committee. This structure ensures that audit findings are presented without filter or bias from management.

The Chief Audit Executive (CAE) communicates directly with the board. They discuss the internal audit plan, resource needs, and significant results. According to The Institute of Internal Auditors, this reporting level is necessary for the internal audit activity to properly fulfill its responsibilities. This direct access gives the board an unvarnished view of the organization’s control environment, enabling better oversight and more informed decisions.

Integrating with Risk Management

The role of internal audit has expanded beyond traditional financial reviews. Today, auditors provide assurance over a wide range of business risks, including those related to cybersecurity, data privacy, and operational resilience. They must look ahead to help the organization prepare for what is next.

This requires auditors to work closely with the company’s risk management function. By aligning their work with key risks, auditors can provide timely insights that guide strategic decisions. This forward-looking approach helps leaders understand and address new and emerging risks before they become major problems. This integration makes the audit function a strategic partner in protecting organizational value.

Maintaining Continuous Audit Readiness

In a complex regulatory environment, waiting for an annual audit is no longer enough. Organizations must be prepared for scrutiny at all times. Internal auditors support this goal by helping to foster a state of continuous audit readiness. This means ensuring that controls are operating effectively every day, not just in the weeks leading up to an audit.

Achieving this requires auditors to develop expertise in new technologies and data analytics. They must be able to test controls within automated systems and analyze large datasets to identify anomalies. As ISACA notes, this technical knowledge is vital for addressing emerging audit challenges and confirming that internal controls are accurate and reliable on an ongoing basis.

Related Articles

Internal Auditing Career FAQs

Table of Contents

Mike Reeves, PhD

Mike is a key figure at the intersection of psychology and technology. He has created and managed algorithms and decision-making tools used by more than half of the Fortune 100.