Article

A Practical Guide to Define Risk Tolerance

Mike Reeves, PhD

|

Updated on

|

Created on

Operating without clear risk boundaries exposes an organization to predictable and preventable failures. Strategic projects become misaligned with the company's financial reality, leaders make reactive decisions during market swings, and critical compliance gaps are left open. These issues are not random; they often stem from a single root cause: a failure to formally define risk tolerance. Ignoring this foundational step is a strategic error with significant consequences. This article explains why a vague approach to risk leads to portfolio misalignment and behavioral mistakes, and how establishing clear limits is essential for building a resilient and well-governed organization.

Key Takeaways

Distinguish between willingness and ability: True risk tolerance requires balancing your cultural appetite for risk with your actual financial and operational capacity to handle setbacks. A strategy is only effective when these two factors are aligned.

Use risk tolerance to guide GRC work: A clear definition of risk tolerance is a practical tool for governance, risk, and compliance teams. It helps focus audit scope, prioritize compliance activities, and align daily decisions with strategic goals.

Treat risk tolerance as a dynamic measure: An organization's risk profile is not static; it changes with market conditions, company growth, and strategic shifts. Your risk tolerance must be reviewed regularly to keep your GRC framework relevant and effective.

What Is Risk Tolerance?

Risk tolerance is the level of risk an organization is willing to accept in pursuit of its objectives. It defines how much uncertainty or potential loss is acceptable before action is needed. This concept is a core part of any governance, risk, and compliance (GRC) framework, guiding decisions from strategic planning to daily operations.

Understanding risk tolerance involves looking at both the organization's mindset and its actual financial and operational limits. It’s not just about what leaders feel comfortable with; it’s also about what the business can realistically handle. A clear definition of risk tolerance helps align the entire organization, ensuring everyone makes decisions within established boundaries.

Willingness vs. Ability

Risk tolerance has two distinct parts: the willingness to take risks and the ability to do so. Willingness is about the organization's culture and strategic appetite. It reflects how comfortable leadership and stakeholders are with uncertainty. Some companies thrive on bold moves, while others prefer a more cautious approach.

Your ability to take risks, however, is based on your financial and operational reality. It is the capacity to absorb losses without threatening the organization's survival. A company with strong cash reserves and a diverse revenue stream has a greater ability to handle risk than a startup operating on thin margins. According to financial services firm Merrill Lynch, separating these two ideas is critical. A high willingness to take risks combined with a low ability can lead to poor outcomes.

Risk Tolerance vs. Risk Capacity

While often used together, risk tolerance and risk capacity are different. Risk tolerance is the amount of risk an organization chooses to accept. It is a strategic decision that sets the boundaries for day-to-day activities. Think of it as the acceptable level of variance around specific business objectives.

Risk capacity, on the other hand, is the maximum amount of risk the organization can possibly bear. As explained by Riskonnect, capacity is an objective ceiling. Exceeding it could lead to severe consequences, such as insolvency or a major compliance failure. While tolerance is a guideline, capacity is a hard limit. Effective GRC programs define their risk tolerance well below their total risk capacity to ensure a safe operating margin.

What Are the Types of Risk Tolerance?

Risk tolerance exists on a spectrum, but it is often grouped into three main categories: conservative, moderate, and aggressive. Understanding where your organization falls on this spectrum is the first step toward building a coherent risk management strategy. These categories provide a shared language for leaders, board members, and audit teams to discuss how much uncertainty the organization is prepared to handle in pursuit of its objectives.

While these terms originate in personal investing, they apply directly to corporate governance. A company’s risk tolerance influences everything from its budget for compliance programs to its appetite for entering new markets. For a Governance, Risk, and Compliance (GRC) leader, identifying the organization’s type is not just an academic exercise. It defines the boundaries for strategic decisions, guides the scope of internal audits, and sets expectations for control environments. A clear understanding of the organization's risk tolerance ensures that compliance efforts are aligned with business goals, rather than working against them.

Conservative

A conservative risk tolerance prioritizes the preservation of capital and stability over the potential for high returns. Organizations with this profile are generally risk-averse. They focus on protecting existing assets, maintaining their reputation, and ensuring predictable performance. This approach often involves robust internal controls, comprehensive compliance programs, and a cautious approach to new ventures or technologies.

According to the Canadian Investment Regulatory Organization, individuals with this profile prefer stability and may hold more secure assets. In a corporate setting, this translates to a business that avoids volatile markets and invests heavily in proven processes. For GRC leaders, a conservative stance means the organization will likely support thorough audits and expect few control failures. The primary goal is to minimize downside risk, even if it means forgoing some opportunities for growth.

Moderate

A moderate risk tolerance represents a balanced approach. Organizations in this category are willing to accept a calculated level of risk to achieve growth. They seek a mix of stability and opportunity, creating a diversified strategy that does not lean too heavily in one direction. This balanced perspective allows them to innovate and expand while maintaining a strong foundation of risk management and compliance.

This middle-ground approach involves taking on some uncertainty in exchange for reasonable returns. For a business, this could mean adopting new software after it has been vetted or expanding into adjacent markets. A GRC leader in a moderate-risk organization will focus on creating a risk appetite statement that enables strategic initiatives while keeping key exposures within acceptable limits. The control environment is designed to be effective but also efficient, supporting business agility.

Aggressive

An aggressive risk tolerance means an organization is comfortable with significant uncertainty in the pursuit of high rewards. These organizations often operate in fast-moving industries where innovation and market capture are critical for survival. They are willing to embrace risk for a competitive edge. This is reflected in their strategic decisions, operational speed, and lean organizational structures.

This high tolerance for risk is often necessary for growth. As CIRO notes for investors, this can mean allocating a substantial portion of resources to higher-risk ventures. For a company, this might look like being the first to market with a new technology or making a large acquisition in an emerging field. GRC leaders in these environments must focus on managing high-impact risks and building resilience. The goal is not to eliminate risk but to understand it, manage it intelligently, and ensure the organization can withstand potential setbacks.

What Factors Shape Risk Tolerance?

Risk tolerance is not a fixed trait. It is a dynamic characteristic shaped by a combination of personal circumstances, knowledge, and psychological factors. Understanding these elements helps governance, risk, and compliance (GRC) leaders create more effective risk management frameworks. Four key factors influence an individual's or an organization's approach to risk.

Age and Investment Timeline

Time is one of the most significant factors in determining risk tolerance. A longer investment timeline provides more opportunity to recover from potential market downturns. For this reason, younger individuals or organizations in the early stages of a long-term project can often afford to take on more risk. They have more time to make up for any short-term losses.

Conversely, those with shorter timelines near a financial goal must be more conservative. A significant loss could be detrimental with less time to recover. The ability to withstand market volatility is directly related to the time you have available.

Financial Stability

Your current financial situation directly impacts your ability to take on risk. A strong financial foundation, including stable income, savings, and low debt, creates a cushion to absorb potential losses. This increases your capacity for taking calculated risks. This factor is not static.

Your financial ability to assume risk can change over time. A promotion or a change in business revenue can alter your stability. Regularly assessing your financial health is crucial for keeping your risk strategy aligned with your actual capacity.

Investment Knowledge

The more you understand investments and market behavior, the more comfortable you may become with risk. Studies show a positive link between financial literacy and financial risk tolerance. Knowledge helps demystify volatility and provides confidence for informed decisions.

For GRC leaders, this highlights the importance of continuous education for their teams. An organization that understands the risks it faces is better equipped to manage them. Knowing your risk tolerance helps you choose strategies that match your long-term goals.

Emotional Response to Volatility

Beyond logic and numbers, risk tolerance has a strong psychological component. Your innate willingness to take risks is a personal trait that often remains consistent. However, market conditions can test anyone's resolve. Risk tolerance often feels higher when markets are rising and lower during periods of volatility.

Understanding your emotional triggers is key to preventing fear or greed from driving decisions. Acknowledging this human element is critical for building resilient risk management programs.

How to Assess Your Risk Tolerance

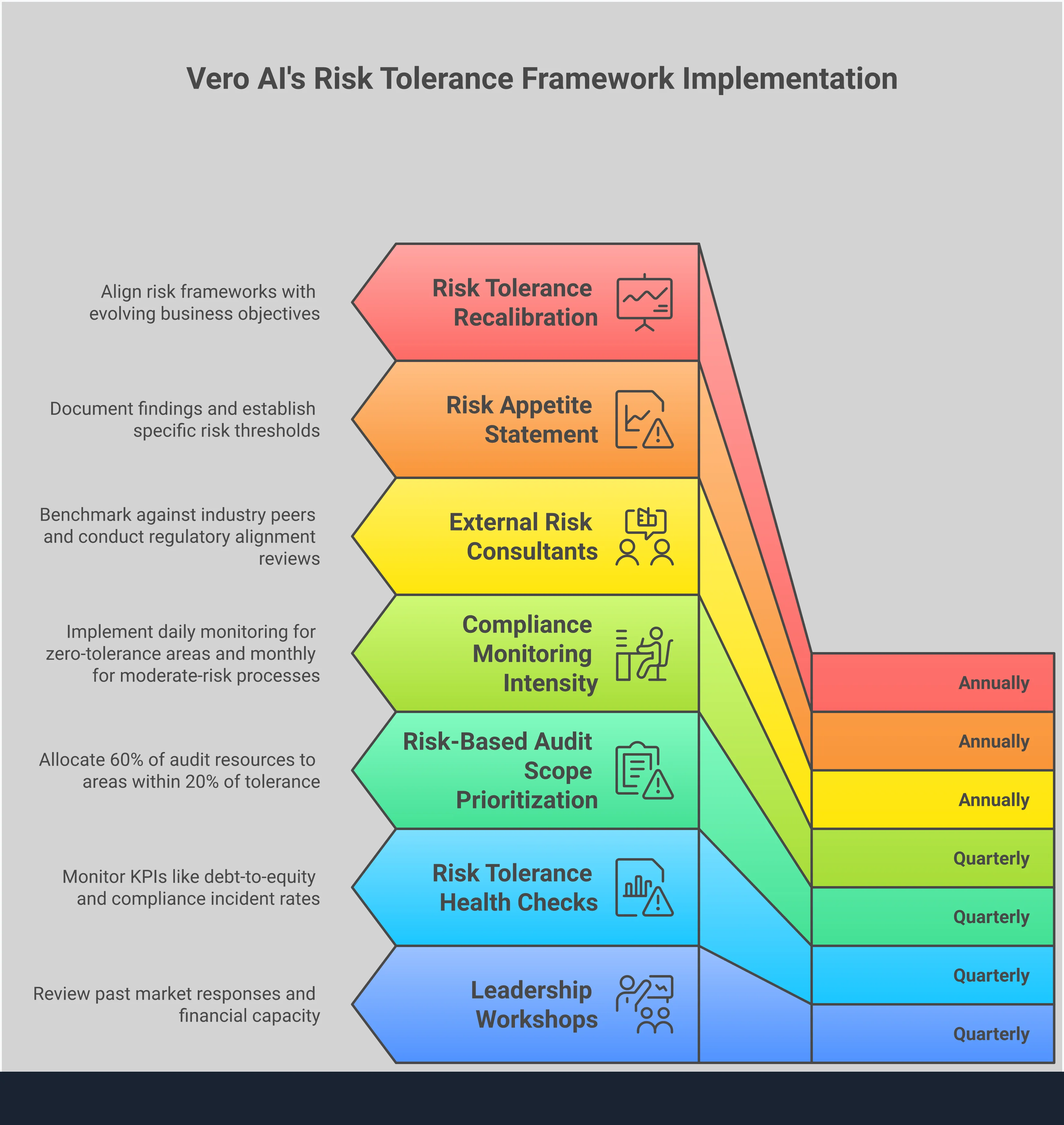

Understanding your organization’s risk tolerance is a critical step in building a strong governance, risk, and compliance (GRC) program. It’s not a one-time task but an ongoing evaluation. A clear assessment helps you align your strategic decisions with your company’s capacity for risk. Three common methods can help you define and measure your organization's risk tolerance: structured questionnaires, internal self-evaluation, and professional risk profiling. Each approach provides a different lens for viewing risk, and using them together creates a more complete picture.

Risk Assessment Questionnaires

Risk tolerance questionnaires are structured tools that help quantify an organization's willingness to accept risk. These surveys use a series of targeted questions to gauge how leaders and teams feel about different risk scenarios and potential outcomes. For example, a question might ask you to choose between a lower-return project with a high certainty of success and a higher-return project with more uncertainty. The collective answers provide a data-driven baseline for your company’s risk profile. This process helps standardize risk conversations across departments and ensures everyone is working from a shared understanding of acceptable risk levels.

Self-Evaluation

Self-evaluation is a more qualitative process that involves deep reflection on your organization's goals and values. This often takes the form of strategic workshops where leadership teams discuss the company’s financial position, long-term objectives, and past responses to market volatility. The goal is to have an honest conversation about what level of risk the organization is truly prepared to handle. This introspective process is fundamental to developing a formal risk appetite statement. This statement acts as a guidepost for decision-making, ensuring that strategic initiatives do not unintentionally expose the company to risks it is unwilling or unable to manage.

Professional Risk Profiling

Professional risk profiling involves engaging external risk management consultants or advisory firms. These experts bring an objective, outside-in perspective to your risk assessment. Their process often includes detailed interviews with key stakeholders, a review of your financial statements, and a comparison of your risk posture against industry benchmarks. A professional assessment can help validate your internal findings and uncover blind spots you might have missed. This external view is especially valuable for aligning your risk tolerance with the expectations of regulators, auditors, and the board of directors, ensuring your GRC framework is both robust and defensible.

Why Is Risk Tolerance Important for Success?

Understanding and defining risk tolerance is fundamental to strategic success. For governance, risk, and compliance (GRC) leaders, it is not just an abstract concept; it is the foundation upon which sound decisions are made. A clearly articulated risk tolerance provides a framework for consistent action, helping teams balance opportunity with caution. It ensures that everyone, from the board to operational managers, is working with the same set of assumptions about which risks are acceptable in the pursuit of organizational goals. Without this clarity, an organization may act too cautiously and miss growth opportunities, or too aggressively and face preventable setbacks. A well-defined risk tolerance aligns strategy, prevents reactive decision-making, and keeps the entire organization focused on its long-term objectives.

Align Investment Strategies

Risk tolerance helps you select strategies and allocate resources that match your organization's comfort level. It measures how much market volatility or potential loss an organization is willing to accept in exchange for greater potential returns. This concept is often called the "sleep at night test" in personal finance, but it applies equally to corporate governance. Investments with a chance for higher returns usually come with a higher chance of loss. By understanding your organization's specific risk tolerance, you can make informed decisions that align with both its growth ambitions and its operational stability, ensuring you don't take on more risk than the company can handle.

Prevent Emotional Decisions

A formal risk tolerance framework serves as a critical guardrail against emotional, reactive decision-making. An organization's willingness to take risks is often stable, but its financial or operational ability to do so can change based on market conditions or internal events. When leaders consider both willingness and ability, they can choose investments and projects that are sustainable. During periods of high stress or unexpected opportunity, a pre-defined risk tolerance prevents leaders from making impulsive choices based on fear or overconfidence. It anchors the decision-making process in established principles, promoting consistency and protecting the organization from behavioral mistakes that could derail its long-term strategy.

Achieve Financial Goals

A clear understanding of risk tolerance is essential for reaching long-term financial and strategic goals. It allows leaders to choose strategies, assets, and project sizes that fit the organization's objectives. If the goal is aggressive growth, the risk tolerance will need to be higher to match. If the priority is stability and capital preservation, a more conservative tolerance is appropriate. By defining how much risk you can handle, you can build a strategic plan that takes calculated risks necessary for growth without exposing the organization to potential failures it cannot withstand. This alignment ensures that every major decision contributes directly to achieving your ultimate objectives.

How Risk Tolerance Impacts Internal Audit and Compliance

An organization’s risk tolerance is not just a theoretical concept for the board. It directly shapes the day-to-day work of internal audit and compliance teams. When risk tolerance is clearly defined, it provides a practical framework for prioritizing resources, focusing on material risks, and aligning activities with strategic goals. This clarity helps teams move beyond simple checklists to become true strategic partners in the business.

Guide Audit Scope

A well-defined risk tolerance tells internal auditors where to focus their attention. Instead of trying to audit everything equally, teams can concentrate on areas where the organization is closest to its risk limits. This risk-based approach makes the audit process more efficient and valuable. It ensures that audit resources are applied to the most significant threats and opportunities facing the business.

The Institute of Internal Auditors (IIA) emphasizes the need for auditors to understand risk tolerance to guide their activities. By aligning the audit plan with the company's stated tolerance levels, auditors can provide more relevant assurance to the board and senior management. This alignment helps confirm that risk management processes are working as intended and are consistent with the organization's goals.

Strengthen Compliance Posture

Risk tolerance also provides critical context for compliance programs. Meeting regulatory requirements is not just about avoiding fines; it is a key part of managing risk. A company’s tolerance for compliance risk influences how it invests in controls, training, and monitoring. For example, an organization with a low tolerance for data privacy risk will implement more stringent controls than one with a higher tolerance.

This approach helps build a cyber risk management program that addresses both security threats and regulatory obligations. When compliance is viewed through the lens of risk tolerance, it becomes a strategic function. It helps protect the organization from harm while supporting its overall objectives, rather than being seen as a simple cost of doing business.

Improve Risk Communication

A clearly articulated risk tolerance creates a common language for discussing risk across the organization. It helps everyone from the front lines to the boardroom understand the boundaries for acceptable risk-taking. This shared understanding is essential for effective governance, risk, and compliance (GRC). When every department understands its role in managing risk, the entire organization becomes more resilient.

Successful internal audits depend on this clarity. According to V-Comply, effective risk management requires clear communication of risk tolerance to ensure operational activities align with organizational goals. This communication helps stakeholders understand their responsibilities, leading to better decision-making and a more consistent approach to managing risk throughout the business.

What Happens When You Ignore Risk Tolerance?

Ignoring risk tolerance is not a passive oversight; it is an active choice with significant consequences. For governance, risk, and compliance (GRC) leaders, this choice can undermine the very foundation of a stable and successful organization. When a company operates without a clear understanding of its risk boundaries, it exposes itself to predictable and preventable failures. These failures are not isolated incidents. They create a domino effect that can impact financial stability, strategic direction, and legal standing. GRC leaders are responsible for building the frameworks that prevent these issues, making a clear definition of risk tolerance a non-negotiable starting point.

The consequences manifest across the business. Strategic initiatives may not align with the company's actual capacity for risk, leading to wasted resources and failed projects. During market stress, leaders may make reactive, emotional decisions that harm long-term growth. Most critically for GRC professionals, a poorly defined risk tolerance can lead directly to compliance gaps and regulatory penalties. Understanding what happens when risk tolerance is ignored is the first step toward building a more resilient and well-governed organization. It provides the context needed to advocate for clear policies and robust internal controls that truly reflect the company's goals.

Portfolio Misalignment

When an organization ignores its risk tolerance, it often develops a portfolio of projects and investments that is misaligned with its strategic goals. This misalignment creates unnecessary stress, as the company may be exposed to risks it is not prepared to manage. For example, a conservative company that invests heavily in speculative technology projects operates outside its comfort zone. When challenges arise, the leadership team may lack the experience or conviction to see the project through, leading to poor decisions and wasted capital. A clear understanding of what risk tolerance is ensures that strategic bets are consistent with the organization's ability to absorb potential losses and uncertainty.

Behavioral Mistakes

A poorly defined risk tolerance makes an organization vulnerable to impulsive decisions, especially during periods of volatility. Without clear guardrails, leadership may react to market shifts based on fear or greed rather than strategy. This can lead to common behavioral mistakes, such as abandoning long-term initiatives at the first sign of trouble or chasing trends without proper due diligence. These reactive choices can destroy value and undermine financial objectives. A well-understood risk tolerance acts as an anchor, helping leaders stay focused on long-term goals instead of getting distracted by short-term noise. It provides a framework for making consistent, rational decisions under pressure.

Compliance and Regulatory Risk

For GRC leaders, one of the most direct consequences of ignoring risk tolerance is an increased risk of compliance failures. Without a clear understanding of its risk appetite, an organization cannot effectively prioritize its compliance efforts. It may fail to allocate sufficient resources to mitigate critical regulatory requirements, creating significant vulnerabilities. This oversight can lead to legal penalties, fines, and lasting reputational damage. A defined risk tolerance is a cornerstone of effective regulatory compliance risk management, as it guides the design of internal controls and ensures that the compliance program is aligned with the organization’s most significant threats.

How to Match Investments to Your Risk Profile

Once you understand your risk tolerance, you can build an investment strategy that aligns with it. This process involves translating your personal comfort with risk into a tangible portfolio. The key is to focus on three core practices: asset allocation, investment selection, and regular portfolio rebalancing. Each step helps ensure your financial plan supports your goals without causing unnecessary stress.

Asset Allocation

Your asset allocation is the mix of different investments, like stocks, bonds, and cash, in your portfolio. This mix is the primary driver of your returns and your risk level. According to research from Merrill Lynch, a portfolio with 100% stocks has a high average return but also carries the potential for significant losses in a bad year.

To find the right balance, consider your time horizon. If you are investing for a long-term goal like retirement, you have more time to recover from market downturns. This allows you to hold a higher percentage of stocks, even if you are naturally cautious. A shorter timeline requires a more conservative allocation to protect your principal.

Investment Selection

After setting your asset allocation, you can choose specific investments. This decision should be based on both your willingness and your ability to take on risk. Willingness is your emotional comfort with market fluctuations. Ability relates to your financial capacity to withstand losses without derailing your goals.

For example, you might have a high willingness to take risks. But if you need the money in two years for a down payment, your ability is low. In this case, financial experts suggest choosing safer investments like bonds or cash equivalents. Aligning your investment selection with both factors helps you build a portfolio that is both psychologically comfortable and financially sound.

Portfolio Rebalancing

Your financial situation and the market are always changing. Because of this, your investment portfolio needs regular check-ups. Portfolio rebalancing is the process of adjusting your asset mix back to its original target.

For instance, if stocks perform well, they may grow to represent a larger portion of your portfolio than you initially planned. This shift could expose you to more risk than you are comfortable with. By selling some stocks and buying other assets, you can realign your portfolio with your risk tolerance. Regularly reviewing your investments ensures your strategy remains consistent with your long-term financial goals as your life evolves.

Common Challenges in Assessing Risk Tolerance

Defining risk tolerance is a critical first step, but applying it consistently across an organization presents several hurdles. Governance, risk, and compliance (GRC) leaders often face challenges that can undermine even the most well-defined framework. These obstacles typically involve aligning risk tolerance with business strategy, ensuring clear communication from the board to the front lines, and adapting to a constantly changing regulatory landscape. Addressing these issues is fundamental to building a resilient and effective risk management program.

Aligning with Organizational Goals

Many organizations struggle to connect their risk tolerance directly to their core business goals. A risk framework can become a simple checklist exercise if it does not support strategic objectives. Different departments often have competing priorities, which can lead to inconsistent applications of risk tolerance. For example, a sales team might accept risks that a legal or finance team would reject. To address this, many companies are adopting tools for governance, risk management and compliance (GRC) to better support their programs, as noted by KPMG International. This alignment helps ensure that risk management enables, rather than hinders, sustainable growth.

Closing Communication Gaps

A clearly defined risk tolerance is ineffective if it is not communicated properly throughout the organization. Gaps often exist between the board’s high-level directives and the daily decisions made by operational teams. Internal audit plays a critical role in bridging this divide. The Institute of Internal Auditors (IIA) has standards that emphasize the need for clear communication between auditors and management on risk appetite. As the Harvard Law School Forum on Corporate Governance highlights, this dialogue is essential. Without it, employees may not understand how their individual actions contribute to the organization's overall risk posture.

Monitoring Evolving Standards

The risk landscape is not static. New regulations, market shifts, and technological changes constantly introduce new threats and opportunities. A significant challenge for GRC leaders is keeping the organization's risk tolerance framework current and relevant. This requires continuous monitoring of both the external environment and internal operations. Many organizations use established risk management frameworks to help structure this process. Regularly reviewing and adjusting risk tolerance ensures that the company remains compliant and prepared for emerging challenges, rather than reacting to them after they have already occurred.

How Risk Tolerance Changes Over Time

Risk tolerance is not a static measure. It is a dynamic attribute that shifts based on both internal priorities and external conditions. For governance, risk, and compliance (GRC) leaders, recognizing this fluidity is essential for building a resilient and adaptive risk management program. An organization's appetite for risk can change with its strategic goals, financial health, and the broader economic environment. What seems like an acceptable risk one quarter may become unacceptable the next.

This requires a continuous approach to risk assessment, not just a one-time evaluation. By understanding the factors that cause risk tolerance to evolve, audit and compliance teams can better anticipate changes and adjust their strategies accordingly. This proactive stance helps ensure that the organization's controls and risk mitigation efforts remain aligned with its current objectives and operating reality. A company's risk profile is shaped by its journey, its reaction to market forces, and its commitment to ongoing self-assessment. Key drivers of this change include organizational life stages, market experiences, and the practice of regular assessment.

Life Stage Transitions

An organization's stage of development heavily influences its ability and willingness to take on risk. A pre-IPO company, for example, might accept higher risks to achieve rapid growth and capture market share. Its focus is on scaling quickly. In contrast, a mature public company often prioritizes stability, shareholder value, and regulatory compliance, leading to a more conservative risk posture.

As financial advisors at Merrill Lynch note, the ability to take risks depends on factors like your timeline and the importance of your goals. For a business, this translates to its capital reserves, strategic timelines, and the criticality of its objectives. GRC leaders must map the company's current business lifecycle stage to its risk framework.

Market Experience

External market conditions create significant shifts in an organization's risk tolerance. During periods of economic growth, companies may feel more confident. They might increase their risk appetite to fund innovation or expand into new territories. Their tolerance for risk is higher when the market outlook is positive.

Conversely, during a recession or periods of high volatility, the focus often shifts to preservation. Companies may pull back on speculative projects and tighten controls to protect assets and maintain operational stability. As ThinkAdvisor points out, risk tolerance often falls when markets are declining. This dynamic relationship between market sentiment and corporate risk-taking requires continuous monitoring from compliance and audit teams.

Regular Assessment and Adjustment

Because risk tolerance is fluid, it requires consistent evaluation. A "set it and forget it" approach can lead to a dangerous misalignment between a company's risk framework and its actual operations. GRC leaders should build processes for periodically reviewing and recalibrating the organization's risk tolerance.

This process should align with key business cycles, such as annual strategic planning or quarterly financial reviews. It should also be triggered by significant events, like a merger, a new regulatory mandate, or a major cyber incident. As one financial expert advises, you should check your risk tolerance often because goals and timeframes change. This ensures the governance, risk, and compliance program remains relevant and effective.

Related Articles

Risk Tolerance FAQs

Table of Contents

Mike Reeves, PhD

Mike is a key figure at the intersection of psychology and technology. He has created and managed algorithms and decision-making tools used by more than half of the Fortune 100.