Article

SOX vs SOC Compliance: Key Differences Explained

Mike Reeves, PhD

|

Updated on

|

Created on

Many organizations treat the Sarbanes-Oxley Act (SOX) and System and Organization Controls (SOC) reports as entirely separate initiatives. This approach creates redundant work, as audit teams chase the same control owners for similar evidence to satisfy different frameworks. While their ultimate goals are distinct, many of the underlying controls for IT, security, and change management are the same. The path to a more efficient program starts with understanding both the differences and the common ground in SOX vs SOC compliance. This article explores how you can map overlapping controls, adopt an integrated approach, and use technology to test once for multiple compliance obligations.

Key Takeaways

SOX is a requirement, SOC is a choice: The Sarbanes-Oxley Act is a mandatory federal regulation for public companies focused on financial reporting. System and Organization Controls reports are voluntary audits that service organizations use to build customer trust.

The audience determines the risk: Sarbanes-Oxley compliance protects investors, so failure can result in legal penalties from regulators. A System and Organization Controls report provides assurance to customers, so non-compliance primarily risks lost business and damaged client relationships.

Integrate controls to reduce duplicate work: Many IT and security controls can satisfy both frameworks. By mapping these overlaps and using technology to automate testing, you can test a control once and use the evidence for multiple audits, saving significant time and effort.

Automate SOX Testing and Produce Audit-Ready Workpapers 👉🏽 Get the SOX Solutions brief

What Is SOX Compliance?

The Sarbanes-Oxley Act of 2002 (SOX) is a United States federal regulation that applies to all publicly traded companies. Congress passed this act in response to major accounting scandals that eroded public trust in corporate financial statements. The main purpose of SOX is to prevent corporate fraud and improve the accuracy and reliability of financial reporting. The rules apply to U.S. public companies and international companies that have registered equity or debt securities with the U.S. Securities and Exchange Commission.

At its core, the Sarbanes-Oxley Act holds corporate executives more accountable for their company's financial records. It established new standards for corporate boards, management, and public accounting firms. According to compliance resource Optro.ai, the act was "created to stop company fraud and make sure financial reports are honest." This requires companies to implement and maintain strict internal controls. These controls are designed to protect shareholders and the general public from accounting errors and fraudulent practices. The U.S. Securities and Exchange Commission (SEC) is responsible for enforcing the Sarbanes-Oxley Act. The regulation fundamentally changed how public companies handle their financial disclosures and corporate governance, creating a new era of transparency. It also created the Public Company Accounting Oversight Board (PCAOB) to oversee the audits of public companies.

Key SOX Requirements

The Sarbanes-Oxley Act has several core requirements. Companies must establish and maintain a framework of internal controls. These are the rules and processes that ensure financial reports are accurate. A company's management team is directly responsible for the effectiveness of these controls.

According to CMIT Solutions, compliance involves three main actions. Companies must "implement appropriate internal controls, document those controls in a way auditors can verify, and pass an independent annual audit." This documentation is a critical piece of the process. It provides the evidence that controls are designed correctly and operating as intended. An external auditor then reviews this evidence and provides an independent opinion on the company's financial statements and internal controls.

Understanding the SOX 404 Mandate

Section 404 is one of the most significant parts of the Sarbanes-Oxley Act. It requires a company's management to assess and report on the effectiveness of its internal controls over financial reporting. This is not a one-time check. It is an annual requirement that involves extensive testing and documentation.

This process can be complex. As consulting firm Plante Moran notes, successful compliance requires the right mix of "governance, culture, and expertise (people) as well as structure (process) and technology." The mandate also extends beyond a company's own operations. Any third-party vendors whose activities support these controls are also part of the scope of a SOX 404 audit. This means companies must also evaluate the controls of their key service providers.

What Is SOC Compliance?

System and Organization Controls (SOC) compliance is a framework established by the American Institute of Certified Public Accountants (AICPA). It provides a way for service organizations to report on their internal controls. These reports give clients and their auditors confidence in the services being provided.

SOC compliance applies to any organization that provides services to other companies, especially those that handle customer data. This includes software-as-a-service (SaaS) platforms, data centers, and managed IT providers. Unlike SOX, SOC is not a government mandate. Instead, it is a voluntary, market-driven standard. Companies obtain a SOC report to build trust with customers, demonstrate security practices, and often to fulfill contractual requirements.

A SOC audit is performed by an independent Certified Public Accountant (CPA). The auditor examines an organization's controls and provides an opinion in a formal report. This report helps a company’s clients understand the risks associated with using that service. There are several types of SOC reports, each designed for a different purpose and audience. The most common are SOC 1, SOC 2, and SOC 3 reports, which address different aspects of a service organization's controls.

Explaining SOC 1, 2, and 3 Reports

SOC reports come in three main varieties, each with a specific focus. A SOC 1 report evaluates a service organization's internal controls over financial reporting. This is important for clients who need assurance that their financial data is handled correctly and that controls are in place to prevent or detect errors in their financial statements.

A SOC 2 report focuses on how a service provider manages and protects client data. The audit is based on five principles known as the Trust Services Criteria: security, availability, processing integrity, confidentiality, and privacy.

A SOC 3 report is a general, public-facing summary of a SOC 2 audit. It confirms that the organization has effective controls related to the Trust Services Criteria. However, it does not include the sensitive operational details found in a full SOC 2 report, making it suitable for marketing purposes.

The Role of the Trust Services Criteria

The Trust Services Criteria (TSC) are the foundation of a SOC 2 audit. Developed by the AICPA, these criteria provide a framework for evaluating the design and effectiveness of an organization's controls. The five criteria are security, availability, processing integrity, confidentiality, and privacy.

One of the main challenges for organizations is correctly interpreting and applying these criteria to their specific systems and processes. For industries like healthcare and finance, SOC 2 compliance is especially important. It helps organizations implement security controls to protect sensitive data, meet industry standards, and build trust with patients and partners. A successful SOC 2 audit demonstrates a clear commitment to safeguarding customer information according to established best practices.

Who Needs to Comply with SOX vs. SOC?

The rules for Sarbanes-Oxley and System and Organization Controls reports apply to different types of organizations. One is a federal requirement for public companies, while the other is a standard for service providers. Understanding which framework applies to your business is the first step in building a compliance strategy.

Who Must Comply with SOX?

The Sarbanes-Oxley Act (SOX) is a United States federal requirement. It applies to all publicly traded companies. The act was created to protect investors by making corporate financial disclosures more accurate and reliable.

If your company is listed on a U.S. stock exchange, you must comply with SOX. This is not optional. The regulation holds senior executives personally responsible for the accuracy of financial data. While SOX is mandatory for public companies, some private businesses choose to adopt its practices. This helps them prepare for a future public offering or sale and demonstrates strong internal controls to potential investors.

Who Needs a SOC Report?

Unlike SOX, a System and Organization Controls (SOC) report is not required by a federal mandate. Instead, the need for a SOC report is typically driven by business and customer demands. These reports are for service organizations that manage sensitive customer data. This includes companies that provide software as a service (SaaS), cloud computing, or data hosting.

Customers often ask their vendors for a SOC report to verify that their data is handled securely. It has become a standard way for service providers to build trust. A report shows they have effective internal controls in place for security, availability, processing integrity, confidentiality, and privacy.

How Do SOX and SOC Differ?

While both the Sarbanes-Oxley Act (SOX) and System and Organization Controls (SOC) frameworks involve internal controls, they serve different purposes. SOX is a federal regulation focused on the integrity of a public company's financial reporting. SOC is a voluntary reporting framework used by service organizations to show customers how they safeguard data and maintain operational controls. Understanding their distinct goals is key to building an effective compliance strategy.

Focus: Financial Reporting vs. Operational Controls

The Sarbanes-Oxley Act was created to prevent corporate fraud and protect investors. Its focus is narrow and specific: ensuring the accuracy and reliability of a public company's financial statements. SOX requires management to establish and maintain adequate internal controls over the processes that produce these financial reports.

System and Organization Controls reports have a broader operational focus. Developed by the American Institute of Certified Public Accountants (AICPA), SOC reports evaluate how well a service organization manages its systems and processes. Depending on the type of report, this can cover security, availability, processing integrity, confidentiality, and privacy of customer data.

Scope: Internal Controls vs. Third-Party Assurance

SOX compliance is an internal responsibility for all publicly traded companies in the United States. The regulation centers on a company’s own financial controls. Management must personally certify that their financial statements are accurate and that their internal control structure is effective. The audience for this assurance is primarily investors and regulators.

A SOC report, on the other hand, is designed to provide assurance to third parties. Service providers, such as software-as-a-service (SaaS) companies or data centers, obtain SOC reports to demonstrate their control environment to customers. It is an outward-facing document that helps clients validate a vendor's security and operational integrity.

Authority: Regulatory vs. Market-Driven

The authority behind SOX is the U.S. federal government. As a regulation enforced by the Securities and Exchange Commission (SEC), compliance is mandatory for all publicly traded companies. Failure to comply can lead to significant fines and even criminal penalties for corporate executives.

In contrast, SOC compliance is market-driven. It is not a legal requirement. Instead, the demand for SOC reports comes from customers who need assurance that their vendors are managing risks appropriately. For many service organizations, providing a SOC report is a business necessity for building trust and winning contracts.

What Are the Key Requirements for Each Framework?

While both frameworks involve controls and audits, their specific requirements differ significantly. The Sarbanes-Oxley Act (SOX) sets specific rules for public companies, while System and Organization Controls (SOC) reports are based on audits that service organizations voluntarily undergo to provide assurance to their customers.

SOX: Documentation and Testing

The Sarbanes-Oxley Act focuses on the accuracy of financial reporting. Its core requirement is that public companies establish and maintain a system of internal controls over financial reporting (ICFR). These are the specific rules and procedures designed to ensure financial statements are reliable.

Companies must document every control in detail. They also need to test them regularly to prove they are designed and operating effectively. Each year, an independent external auditor must also perform an audit of these controls and issue a formal opinion, providing assurance to investors and regulators.

SOC: Audits and Reporting

System and Organization Controls reports provide assurance about a service organization's systems and processes. Unlike SOX, SOC is not a set of government-mandated rules. Instead, it is a framework for audits performed by a Certified Public Accountant (CPA) firm.

These audits assess an organization's controls related to financial reporting (SOC 1) or operational and security principles (SOC 2). The main requirement is to undergo the audit itself. The outcome is a formal report that the service organization can share with its customers to build trust and demonstrate its commitment to security and operational integrity.

Standards for Managing Evidence

Both SOX and SOC compliance depend on effective evidence management. Auditors require clear proof that controls are in place and functioning correctly. For SOX, this involves collecting evidence for hundreds of controls, from access management logs to change control documentation. For SOC reports, service organizations must provide evidence that supports their assertions about their systems.

Maintaining this evidence requires continuous monitoring and organization. Teams often use specialized software to automate tracking, manage workflows, and prepare for audits. This helps avoid relying on manual spreadsheets and folders, which can be error-prone and time-consuming.

Common SOX and SOC Compliance Challenges

Both Sarbanes-Oxley (SOX) and System and Organization Controls (SOC) programs require significant effort to maintain. While their goals differ, they share common operational hurdles. Most challenges stem from a reliance on manual processes, a shortage of specialized expertise, and the slow adoption of technology. These issues can make compliance feel like a constant uphill battle, consuming time and resources that could be used for more strategic risk management.

The Burden of Manual Testing

Manual testing is the most time-consuming part of SOX and SOC compliance. Teams spend thousands of hours each audit cycle collecting, reviewing, and documenting evidence. This evidence often comes in messy formats like PDFs, complex spreadsheets, and system screenshots. Auditors must manually check each piece of evidence against specific control requirements, a process that is both slow and highly susceptible to human error. This repetitive work not only drains morale but also creates audit risk. Inconsistent testing procedures and documentation gaps can lead to negative findings from external auditors and regulators.

Overcoming Resource and Expertise Gaps

Many organizations struggle to staff their compliance functions adequately. Smaller enterprises often lack the dedicated staff or internal knowledge needed to prepare for a SOC audit. Even larger companies with established internal audit teams face challenges. Skilled auditors often spend their time on tedious, mechanical tasks instead of high-judgment risk analysis. This misuse of talent contributes to burnout and makes it difficult to retain experienced professionals. A successful compliance program requires the right combination of governance, culture, and expertise, but finding and keeping the right people is a persistent challenge.

Integrating Technology for Continuous Monitoring

Periodic, manual testing means control failures are often discovered months after they occur, usually during a stressful year-end audit. Technology offers a path toward continuous monitoring, allowing teams to identify issues in near real-time. Implementing and maintaining controls for access management, logging, and change management requires tools and continuous oversight. By automating these processes, organizations can maintain a constant state of audit readiness. This proactive approach strengthens risk management and transforms compliance from a reactive, year-end scramble into a consistent, ongoing business function.

What Are the Consequences of Non-Compliance?

Failing to comply with either Sarbanes-Oxley (SOX) or System and Organization Controls (SOC) standards carries significant risks. While both can lead to financial and reputational damage, the nature of the penalties differs. SOX non-compliance involves legal and regulatory enforcement. SOC non-compliance primarily affects business relationships and market trust. Understanding these consequences is the first step in building a strong compliance program.

SOX: Penalties and SEC Enforcement

The consequences for failing to comply with the Sarbanes-Oxley Act are severe and legally binding. Because SOX is a federal regulation enforced by the U.S. Securities and Exchange Commission (SEC), penalties are not optional. Non-compliance can lead to large fines, criminal charges, and the delisting of a company's stock from public exchanges.

For executives, the stakes are even higher. The regulation holds corporate officers directly accountable for the accuracy of financial reports. According to research from Exabeam, this means non-compliance can result in "big fines and even jail time for company leaders." These strict enforcement actions are designed to protect investors by ensuring financial transparency and accountability.

SOC: Impact on Business Relationships

Unlike SOX, System and Organization Controls (SOC) compliance is not mandated by a government body. Instead, it is driven by market and customer demands. The consequences of non-compliance are commercial rather than legal. As compliance software provider Optro notes, "Non-compliance with SOC usually results in lost business opportunities."

Many companies will not partner with a service organization that cannot produce a clean SOC 2 report. It serves as essential proof that you have the proper controls in place to protect their data. Lacking this report can disqualify you during procurement, damage client trust, and cause you to lose contracts to competitors who can provide that assurance.

Understanding Reputational and Financial Risks

Beyond direct penalties, non-compliance with either framework can cause lasting reputational harm. A Sarbanes-Oxley failure signals to investors and the public that a company's financial controls are weak. This can erode confidence and potentially lower its stock value. A SOC 2 failure tells customers and partners that their data may not be safe, which can be devastating for a service organization.

These events create significant financial fallout. The costs include not only fines or lost contracts but also the expense of remediation, higher insurance premiums, and shareholder lawsuits. Both frameworks are designed to build trust, and failing to meet their standards breaks that trust with the stakeholders who matter most.

How to Streamline SOX and SOC Compliance

Managing Sarbanes-Oxley Act (SOX) and System and Organization Controls (SOC) programs can feel like running two separate races. Each has its own finish line and set of rules, often leading to duplicated effort and audit fatigue. Teams find themselves chasing the same evidence from the same control owners for different audits, creating friction and wasting valuable time. The cost of this inefficiency is not just financial; it also pulls talented auditors away from strategic risk analysis and into repetitive administrative work.

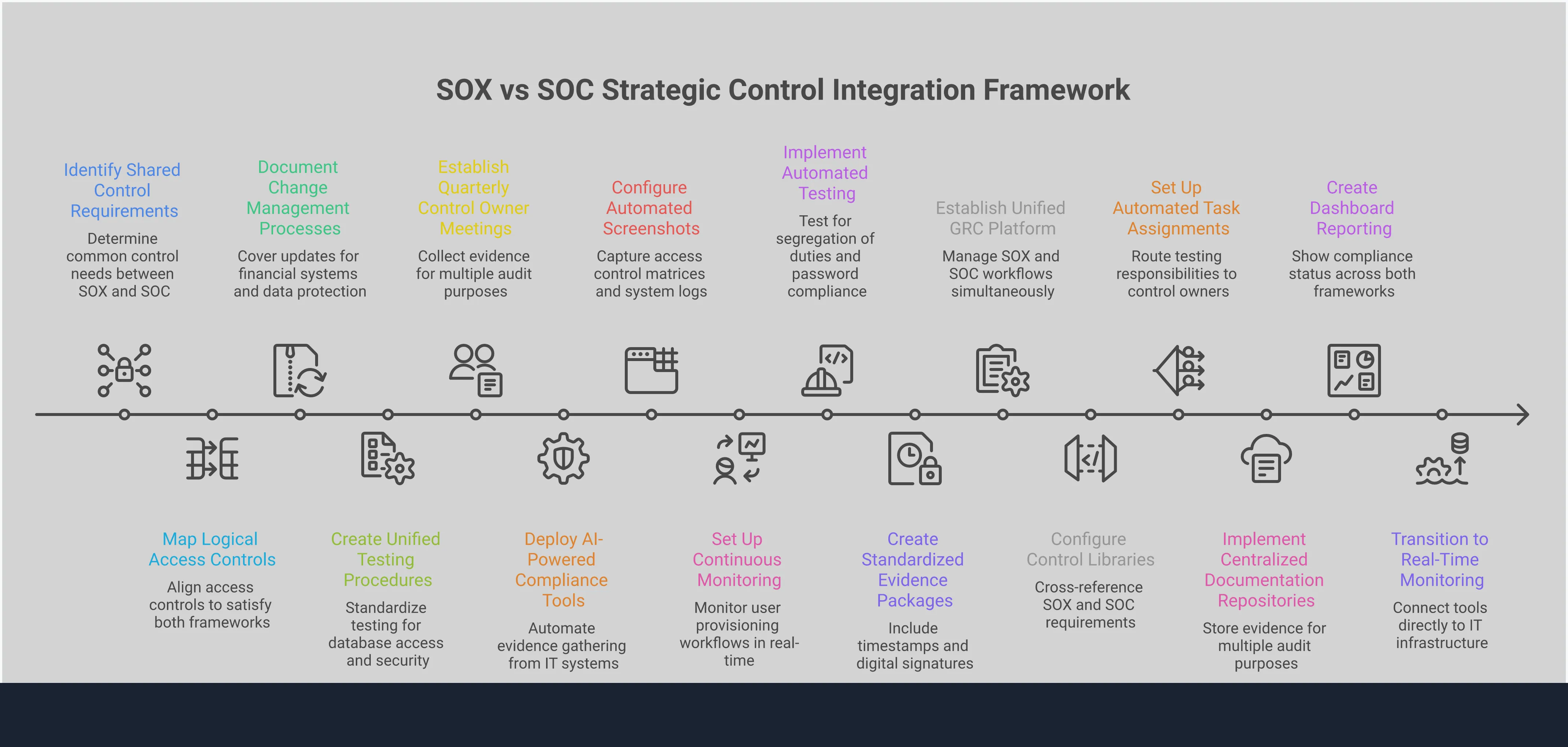

However, many of the underlying control activities for these frameworks are the same. By recognizing the similarities, you can create a more efficient and effective compliance program. A streamlined approach focuses on three key areas. First, you can identify where control requirements overlap between SOX and SOC, allowing you to test a single control and use the evidence for both audits. Second, you can adopt an integrated compliance strategy that treats all your obligations as part of a unified program. Finally, you can use automation in audit to handle the repetitive, manual tasks that consume most of your team's time. Combining these strategies helps you move from a reactive, audit-by-audit cycle to a state of continuous readiness.

Find Overlap in Control Requirements

Many controls required for SOX are also fundamental to a SOC 2 report. For example, controls around logical access, change management, and data security often satisfy requirements for both frameworks. A well-designed control for user access reviews under the SOC 2 Security criteria can also support your Sarbanes-Oxley Act Information Technology General Controls (ITGCs).

Mapping these shared requirements is the first step. By creating a unified control framework, you can test a control once and apply the results across multiple audits. This approach reduces redundant testing efforts and simplifies evidence gathering for your control owners. It turns two separate requests into a single, more efficient one.

Adopt an Integrated Compliance Approach

Finding overlapping controls is a tactical win. Adopting an integrated approach is a strategic one. Instead of managing SOX and SOC in separate silos, you can build a single program to govern them. This requires a combination of the right people, processes, and technology to create a framework that fits your business.

An integrated program provides a single source of truth for your compliance posture. It ensures that controls are applied consistently across the organization. When a regulation or business process changes, you can assess the impact once and update your entire control environment accordingly. This creates a more resilient and adaptable compliance function that can scale with your organization instead of creating more work.

Use Automation and Technology

Manual evidence collection and testing are significant drains on internal audit and compliance teams. These repetitive tasks are often the source of errors and burnout. Technology can automate many of these processes, allowing your team to focus on judgment and strategic risk analysis.

Tools for SOX control automation can handle tasks like gathering evidence, testing samples, and preparing workpapers. This not only speeds up audit cycles but also improves consistency and creates a clear audit trail. By automating routine checks, you can move closer to continuous monitoring. This helps you identify and address control weaknesses as they happen, not just during the year-end audit cycle.

What Tools Support SOX and SOC Programs?

Managing Sarbanes-Oxley (SOX) and System and Organization Controls (SOC) programs involves handling large volumes of evidence and repetitive testing. Technology can help streamline these efforts. The right tools automate manual work, organize documentation, and provide clear visibility into compliance status. Three main categories of software support these programs: GRC platforms, AI-powered automation tools, and continuous monitoring solutions. Each serves a distinct purpose in building a more efficient and reliable compliance function.

GRC and Audit Management Platforms

Governance, Risk, and Compliance (GRC) platforms are foundational tools for many audit teams. They provide a central system for managing compliance activities. These platforms help you document controls, map them to specific regulations like SOX, and track their testing status. For example, a GRC tool can help map control objectives for financial reporting to the exact IT systems and processes involved. This creates a structured framework for organizing the audit process. GRC platforms act as a single source of truth, helping teams manage workflows, assign tasks, and store evidence in one place. They are designed to bring order to complex compliance programs.

AI for Compliance Analytics and Automation

Artificial intelligence adds a layer of automation to compliance testing. AI-powered tools can analyze evidence to determine if it meets control requirements. Instead of manually reviewing hundreds of screenshots or PDF files, auditors can use AI to perform these checks automatically. This technology can interpret complex documents, identify missing information, and flag exceptions for human review. The goal is to streamline documentation and maintain a state of year-round audit readiness. By automating repetitive tasks, these tools free up auditors to focus on higher-level risk analysis and judgment. This leads to faster testing cycles and more consistent results.

Tools for Continuous Monitoring

Continuous monitoring tools shift compliance from a periodic event to an ongoing process. These platforms connect directly to your company’s IT systems to gather and test evidence automatically. Instead of waiting for a quarterly or annual audit, you can get real-time data on how well your controls are performing. This approach helps you remain compliant and audit-ready at all times. For example, a tool could automatically check user access logs every day to ensure that only authorized employees have access to sensitive financial systems. This allows teams to identify and fix control weaknesses as they occur, rather than discovering them months later during an audit.

Which Framework Applies to Your Organization?

Deciding between SOX and SOC compliance is not always an either/or choice. The right framework, or combination of frameworks, depends on your company’s structure, industry, and customer commitments. Understanding the core purpose of each will help you build a strategy that meets both regulatory demands and market expectations.

How to Know if SOX Applies to You

The Sarbanes-Oxley Act (SOX) is a U.S. federal requirement, not an optional standard. It applies to all publicly traded companies in the United States. The act was created to protect investors from corporate fraud by mandating accurate and transparent financial reporting.

If your company is listed on a U.S. stock exchange, you must comply with SOX. Private companies are generally not required to follow SOX rules. However, this changes if you are preparing for an Initial Public Offering (IPO) or are acquired by a public company. In those cases, you will need to establish SOX compliance.

How to Assess Your Need for a SOC Report

Unlike SOX, a System and Organization Controls (SOC) report is not required by law. Instead, it is a voluntary report that service organizations use to build trust with their clients. If your company handles sensitive customer data, a SOC report demonstrates that you have effective controls in place to protect it.

Customers often ask for these reports during their vendor due diligence process. There are different types of reports for different needs. A SOC 1 report focuses on controls relevant to a client’s financial reporting. A SOC 2 report evaluates controls based on criteria like security, availability, and confidentiality.

How to Build Your Compliance Strategy

A successful compliance program relies on more than just a checklist. It requires a thoughtful strategy that combines people, processes, and technology. Your approach should start with clear governance and a culture that values internal controls. This foundation helps align your compliance efforts with your overall business goals.

Designing and maintaining the right controls, such as access management and change control, requires expertise and consistent oversight. Many organizations find that automating compliance processes helps them maintain continuous readiness. This allows teams to move beyond manual evidence collection and focus on strategic risk management.

Related Articles

FAQs About SOX vs SOC Compliance

Table of Contents

Mike Reeves, PhD

Mike is a key figure at the intersection of psychology and technology. He has created and managed algorithms and decision-making tools used by more than half of the Fortune 100.