Article

Audit Working Paper 101: The Ultimate Guide

Eric Sydell, PhD

|

Updated on

|

Created on

Every audit tells a story. It begins with a plan, moves through a series of tests and observations, and ends with a final, evidence-based conclusion. The audit working paper is the book where this story is written. It contains the complete narrative of the engagement, capturing the rationale behind every decision and linking each finding to the evidence that supports it. The goal is to create a record so clear and logical that another experienced auditor can read it and arrive at the same conclusion. This article explores how to construct that narrative, from organizing evidence to documenting procedures and meeting critical retention requirements.

Key Takeaways

Document everything to support your findings: Your working papers are the main record that proves your audit opinion is sound and that you followed professional standards.

Create consistent habits for better quality: Standardize your templates and document work in real time to avoid errors and make the review process smoother for everyone.

Automate tasks but prioritize security: Use technology to handle repetitive evidence collection, but ensure you have strong access controls to protect confidential client data and meet retention rules.

What Are Audit Working Papers?

Audit working papers are the documents that record the evidence an auditor collects during an engagement. Think of them as the complete story of the audit, from initial planning to the final conclusion. These records are fundamental to financial audits, internal management reviews, and information systems compliance checks.

The main goal of these papers is to show that the audit was planned and executed correctly. They provide a clear trail of the work performed, the tests conducted, and the evidence that supports the auditor's final opinion. This documentation is crucial for quality reviews and demonstrating adherence to professional standards. Essentially, working papers are the backbone of a defensible and well-executed audit.

Defining Core Components and Purpose

The core purpose of audit working papers is to document the link between the audit procedures performed and the conclusions reached. They serve as the primary record of all work, showing how the audit was planned, supervised, and reviewed. This creates a comprehensive audit trail that another experienced auditor could follow to understand the work and reach the same conclusion.

These documents contain everything from planning memos and risk assessments to test results and client communications. By capturing this information, working papers help auditors organize their findings, support their final report, and facilitate effective review by supervisors or external inspectors.

Differentiating Current vs. Permanent Files

To keep information organized, auditors typically separate working papers into two categories: current files and permanent files. This structure helps streamline the audit process year after year.

The current file contains all documentation relevant to the audit for the specific period under review. This includes the audit plan, trial balances, and evidence from testing. The permanent file holds information of continuing importance across multiple audits. Examples include a company’s articles of incorporation, long-term contracts, and key accounting principles. This distinction between files ensures that foundational knowledge is carried forward, making future audits more efficient.

Why Working Papers Are Essential for Compliance

Audit working papers are more than just administrative records. They form the foundation of a credible and defensible compliance program. These documents provide a clear, detailed account of the audit process from start to finish. They connect the evidence gathered to the conclusions reached, creating a logical trail that can be reviewed by managers, executives, and external regulators.

Well-prepared working papers serve three critical functions. First, they provide the primary support for the auditor's final opinion on a company's financial statements or internal controls. Second, they demonstrate that the audit itself was conducted in accordance with professional standards. Finally, they serve as a crucial record that can protect the auditor and their firm in the event of legal disputes or regulatory inquiries. Each function is essential for maintaining the integrity of the audit process and ensuring that compliance objectives are met with confidence.

Supporting Audit Opinions

An audit opinion is only as strong as the evidence that supports it. Working papers are the principal record that substantiates the auditor's conclusions. They contain all the information gathered, the tests performed, and the judgments made throughout the engagement. According to the Public Company Accounting Oversight Board (PCAOB), these documents provide the main proof that the auditor's report is correct.

Without this detailed documentation, an audit opinion is simply an unsubstantiated claim. Clear and organized working papers allow a reviewer to understand how the auditor arrived at their conclusion. They show the link between specific control tests and the overall assessment of compliance, making the final opinion both credible and defensible under scrutiny from regulators or stakeholders.

Demonstrating Adherence to Standards

Working papers do more than just support the final audit opinion. They also prove that the audit itself was performed correctly. Professional auditing standards require auditors to document their work in a way that shows the engagement was properly planned and supervised.

The documentation must also show that the auditor gained a sufficient understanding of the company's internal controls. Finally, it needs to prove that enough appropriate evidence was collected to form a reasonable basis for their findings. This record is essential for internal quality reviews, peer reviews by other firms, and inspections by regulatory bodies. It confirms the audit was conducted with professional diligence and rigor.

Documenting Evidence for Legal Protection

In a complex regulatory environment, auditors and their firms face potential legal and financial risks. Comprehensive working papers are a critical line of defense. If an audit is ever questioned in a lawsuit or regulatory investigation, these documents serve as the primary evidence of the work performed and the professional care that was taken.

These records are the property of the auditor, not the client, and are kept confidential. They create a detailed timeline of the engagement, capturing the rationale behind key decisions. Regulations often require a specific document retention period, typically seven years or more, because these papers may be needed long after an audit is complete to defend the integrity of the work.

What to Include in Audit Working Papers

Effective working papers tell the complete story of an audit. To build a defensible audit file, you need to include specific elements, organize them logically, and record your work clearly. The goal is a standalone record that another experienced auditor can review to understand the work performed, the evidence gathered, and the basis for your conclusions. This documentation is the primary support for your audit opinion and demonstrates compliance with professional standards.

Key Documentation Elements

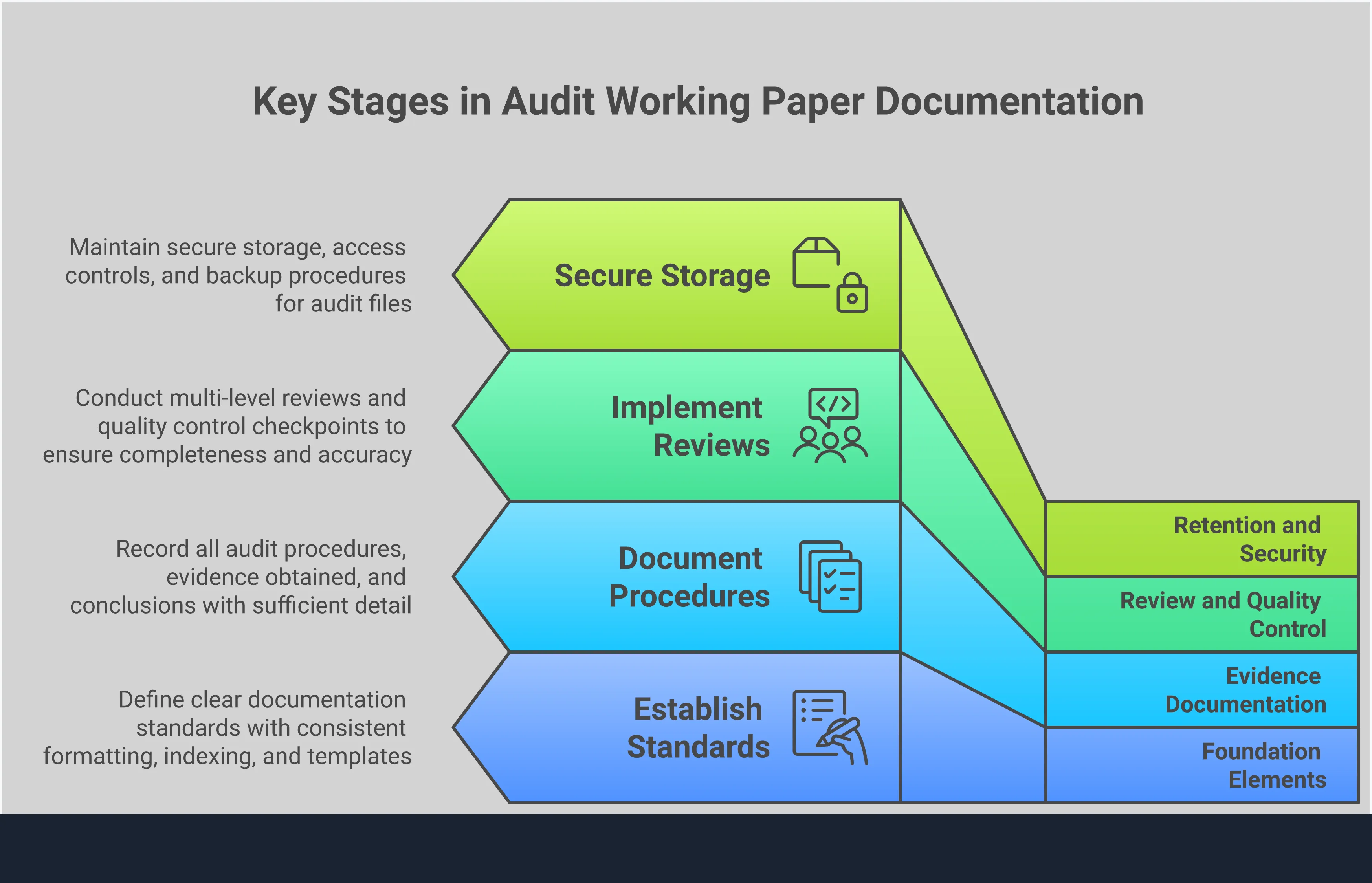

Audit working papers are the documents that record all audit evidence gathered during an engagement. Their main purpose is to show how you arrived at your audit opinion and prove the audit followed all applicable standards. Key elements include the audit plan, risk assessments, descriptions of controls tested, and procedures performed. You should also include copies of relevant client documents and correspondence. Each paper must clearly link the evidence to the specific control being tested, providing a logical path from planning to the final report.

How to Collect and Organize Evidence

A systematic approach to gathering evidence is essential. Auditors must identify, analyze, and document enough information to meet the engagement’s objectives. Developing cohesive working papers from the start helps your team avoid redoing work or making repetitive client requests. This is a core part of efficient audit documentation. Organize evidence logically, often by control objective, using a consistent indexing system so reviewers can trace information. This is especially important for complex evidence like system reports, screenshots, and PDFs, ensuring all support is properly filed.

Recording Procedures and Test Results

Your working papers must show that the audit was properly planned and supervised. This means documenting work as it happens, not weeks later when details are less clear. Each step in the audit program should be signed off as it is performed to create a clear trail. For each test, document the items selected, the nature of the test, and the results. If you find exceptions, describe them clearly and explain their resolution. This detail creates a traceable record that supports your findings and withstands scrutiny from reviewers and inspectors.

Common Challenges with Working Papers

While essential, creating and managing audit working papers presents significant operational hurdles. Teams often struggle with the sheer volume of evidence, the pressure to maintain quality under tight deadlines, and the need for absolute clarity in their documentation. These challenges can lead to inefficiencies, increased audit risk, and burnout among skilled compliance professionals. Overcoming them requires a structured approach to how working papers are created, reviewed, and stored.

Managing High Volume and Organization

The scale of a modern audit generates a massive amount of documentation. For many organizations, preparing for a single audit can consume months of work, placing a heavy burden on compliance and internal audit teams. According to a report from A-LIGN, two-thirds of organizations spend at least three months each year on audit preparation. This extensive time commitment highlights the common challenges of the audit process. Sifting through hundreds or thousands of documents, emails, and system exports makes organization a constant struggle. Without a systematic approach, evidence can be misplaced, versions can get mixed up, and the audit trail can become difficult to follow.

Maintaining Quality Under Pressure

Audit deadlines create a high-pressure environment where the quality of documentation can suffer. When teams are rushed, consistency often becomes the first casualty. Different auditors may have their own documentation styles or preferences, leading to workpapers that are difficult for others to review and understand. This lack of standardization creates inefficiencies and increases the risk of errors. The Journal of Accountancy highlights several strategies for effective audit documentation to combat this, emphasizing that standardized procedures are key. Without them, managers spend excess time on reviews, and the firm exposes itself to greater scrutiny from external auditors and regulators.

Ensuring Clarity and Completeness

In the rush to complete fieldwork, auditors sometimes delay documenting their procedures, planning to "catch up" later. This practice is risky. Postponing documentation can lead to incomplete or inaccurate records because important details are forgotten over time. This often forces auditors to redo work or make follow-up requests to control owners, creating friction and delays. As the Journal of Accountancy notes, developing a cohesive set of working papers as work is performed is critical. In a worst-case scenario, unclear or incomplete documentation could even lead to the recall of an audit report, making real-time, clear documentation essential for a defensible audit trail.

How to Overcome Working Paper Challenges

The challenges of managing audit working papers can feel overwhelming, but they are not insurmountable. By implementing structured processes and clear standards, audit teams can improve the quality, clarity, and organization of their documentation. These strategies focus on creating consistent habits that reduce pressure during critical audit cycles and ensure the final work product is defensible and complete. Adopting these practices helps teams move from a reactive approach to a more proactive and efficient documentation workflow.

Standardize Your Documentation

Consistency is key to clear and reliable working papers. When every auditor documents their findings differently, it creates confusion and slows down the review process. Creating a standardized format for reports and evidence collection ensures everyone follows the same structure. This approach helps minimize confusion and improves the overall quality of the audit. Using templates for common tests and procedures also makes the documentation process faster and more accurate. It allows reviewers to find information quickly and confirms that all necessary steps were completed and recorded properly. A uniform system makes training new team members easier and supports a more efficient workflow for the entire department.

Adopt Real-Time Documentation

It can be tempting to perform audit procedures and save the documentation for later. However, this habit often leads to problems. Waiting to document can result in forgotten details, incomplete evidence, and the need to redo work. Auditors who delay documentation are more likely to make follow-up requests to clients or miss key information. Adopting effective audit documentation practices, like recording findings as you work, creates a more accurate and cohesive set of working papers. This real-time approach saves time in the long run and reduces the risk of errors or omissions in the final audit file.

Implement Quality Review Processes

Working papers are not complete until they have been reviewed. A formal quality review process confirms that the work is accurate, complete, and supports the audit conclusions. This step should involve a supervisor or senior team member who examines the documentation for clarity and adherence to standards. Documented supervisory reviews are a core component of creating effective work papers and demonstrating due professional care. This practice not only improves the quality of the current engagement but also provides valuable feedback for the auditor. It helps foster continuous improvement and builds a stronger, more proficient audit team over time.

Meeting Retention and Confidentiality Requirements

Creating clear and complete audit working papers is only half the process. Your team also has a professional and legal duty to manage them responsibly long after an audit concludes. This responsibility breaks down into two key areas: retaining documents for a specific period and protecting the confidential client information they contain. Failing in either area can lead to regulatory penalties and damage your firm’s reputation. Let's look at how to meet these critical requirements.

Understanding Regulatory Timelines

Regulatory bodies require audit firms to keep working papers for a set amount of time. For public companies in the U.S., the Public Company Accounting Oversight Board (PCAOB) mandates a retention period of seven years from the audit report's release date. This rule ensures that a complete record of the audit exists for future reference. This documentation can be crucial during regulatory inspections or if legal questions arise about the audit years later. Your firm’s internal policies should reflect these external auditing standards to ensure you are always in compliance.

Protecting Sensitive Client Information

While auditors own the working papers they create, the information inside is confidential. You cannot share these documents with outside parties without your client’s explicit permission. The only exceptions are specific legal situations, such as a court order. This principle of confidentiality is a cornerstone of the auditor-client relationship. Breaching it can result in serious professional and legal consequences. Your team must treat all client data with the highest level of care, ensuring it is never disclosed improperly.

Implementing Access Controls and Security

Protecting client information requires more than just a promise; it requires strong security measures. For digital working papers, this means implementing strict access controls to ensure only authorized personnel can view or edit the files. Using encryption for data both in transit and at rest adds another critical layer of security. These practices are fundamental to building a secure information security management system. By limiting access and securing the data itself, you fulfill your duty to keep client information private and safe from unauthorized access.

How to Manage Working Papers Effectively

Managing working papers effectively requires a structured approach that combines clear standards, modern tools, and a commitment to improvement. When your team has a reliable system, they can produce consistent, high-quality documentation that stands up to scrutiny. This system reduces the manual burden on auditors, allowing them to focus on higher-value risk analysis. The following strategies can help your team build a more efficient and defensible process for managing audit working papers.

Develop Standards and Templates

Consistency is the foundation of reliable audit documentation. Standardized templates ensure every team member follows the same format and includes all necessary information, which makes the review process much smoother. According to the Journal of Accountancy, a cohesive set of working papers makes it less likely that an auditor will need to redo work. Your templates should clearly outline the control objective, testing procedures, results, and a conclusion. By standardizing your approach, you create a repeatable process that improves the quality and defensibility of your team's work.

Use Technology and Automation

Manual working papers are prone to errors and difficult to manage at scale. Modern audit teams use technology to automate repetitive tasks and centralize documentation. As Thomson Reuters notes, automation is becoming a standard operating procedure for competitive firms. Platforms for SOX Control Automation can automatically gather evidence, link it to specific controls, and generate structured workpapers. This frees up auditors from manual data entry and organization. Instead, they can focus their expertise on evaluating control effectiveness and identifying risks, making the audit process more strategic.

Establish a Process for Continuous Improvement

Effective working paper management is an ongoing process. Your team should regularly review and refine its documentation practices to adapt to new risks and regulations. The Institute of Internal Auditors suggests that documented supervisory reviews and other feedback can show the proficiency of auditors. After each audit cycle, hold a review meeting to discuss what went well and what could be improved. Analyze review notes to identify common issues. Use these insights to update your templates and training materials, ensuring your team’s processes evolve.

Related Articles

FAQs: Audit Working Paper

Table of Contents

Eric Sydell, PhD

Eric has two decades of experience in enterprise technology and was a founder of Modern Hire, which became part of Hirevue in 2023.