Blog

AI in Accounting and Auditing: A Practical Guide

Mike Reeves, PhD

|

Updated on

|

Created on

Many organizations struggle with the high cost and manual effort of compliance. Audit teams spend thousands of hours each year on repetitive tasks like gathering evidence, reviewing documents, and preparing workpapers for Sarbanes-Oxley (SOX) testing. This process is slow, prone to error, and pulls skilled professionals away from higher-value work. The use of AI in accounting and auditing directly addresses this challenge. By automating the mechanical layers of compliance, these systems allow teams to test 100% of controls continuously. This not only improves accuracy but also helps organizations maintain a constant state of audit readiness, transforming compliance from a periodic burden into a strategic advantage.

Key Takeaways

Shift focus from manual tasks to strategic analysis: AI handles repetitive data collection and review, allowing accountants and auditors to apply their expertise to risk assessment, complex problem-solving, and advisory services.

Move from periodic sampling to continuous monitoring: AI systems can analyze complete datasets as they are generated, providing a real-time view of compliance. This helps teams identify and address control weaknesses much earlier than traditional audits.

Plan for AI adoption beyond the technology: A successful integration requires addressing data quality, training your team for new skills, and selecting tools that provide transparent, auditable results to support your findings.

What Is AI in Accounting and Auditing?

Artificial intelligence (AI) in accounting and auditing refers to systems that perform tasks that once required human judgment. These tools can interpret complex documents, identify patterns in financial data, and evaluate evidence against compliance requirements. Unlike traditional software that follows a rigid set of rules, AI learns from data to make reasoned conclusions. This capability is especially valuable for tasks like Sarbanes-Oxley (SOX) control testing, where evidence comes in many different formats.

For financial professionals, this technology is not about replacing human expertise. It is about augmenting it. AI handles the repetitive, time-consuming aspects of data collection and analysis. This allows auditors and accountants to focus on strategic risk assessment, complex problem-solving, and advising business leaders. By automating the mechanical layers of compliance and financial oversight, AI helps teams work more efficiently and deliver deeper insights. This allows organizations to build more robust AI governance and compliance programs.

What AI Means for Financial Professionals

Many accountants and auditors are considering how artificial intelligence will affect their roles. The primary impact is a shift away from manual, repetitive work. AI is increasingly used to handle tedious tasks like summarizing long documents, matching invoices, and verifying transaction details. This technology acts as a powerful assistant, freeing up professionals from the routine work that often consumes the bulk of their time.

This shift allows financial experts to concentrate on activities that create more value. Instead of spending hours checking samples, an auditor can analyze the anomalies an AI system has flagged across an entire dataset. According to research in The CPA Journal, AI is best viewed as an augmentation tool that enhances the capabilities of human accountants, rather than a full replacement.

Key Technologies: Machine Learning and NLP

Two core technologies drive most AI applications in finance: machine learning and natural language processing. Machine learning (ML) algorithms analyze vast datasets to find patterns, identify outliers, and predict future outcomes. In an audit context, ML systems can review millions of transactions to detect anomalies or potential fraud that would be impossible for a human to spot manually.

Natural language processing (NLP) gives software the ability to read, understand, and interpret human language. This is critical for reviewing unstructured evidence like contracts, emails, and PDF reports. NLP can extract key terms, dates, and figures from these documents to verify compliance with specific controls. Together, ML and NLP allow AI platforms to both process and understand complex financial information.

AI vs. Traditional Automation: What's the Difference?

It is important to distinguish AI from traditional automation, such as Robotic Process Automation (RPA). Traditional automation is based on explicit rules. An RPA bot follows a pre-programmed script to perform a simple, repetitive task, like copying data from a spreadsheet to a financial system. It cannot deviate from its instructions or handle unexpected formats.

AI, on the other hand, is designed to manage variability and make judgments. It can interpret unstructured data, learn from new information, and handle tasks that lack a simple, rule-based solution. For example, while RPA can move a file, an AI system can read the file, determine if it satisfies a control objective, and document its conclusion. As the Journal of Accountancy notes, AI helps auditors do their jobs better by processing huge volumes of information with greater speed and accuracy.

How AI Transforms Accounting Operations

Artificial intelligence is changing the core functions of accounting departments. It moves teams away from manual data handling and toward strategic analysis. By automating routine tasks, AI systems allow financial professionals to focus on judgment-based work that adds more value to the organization. This operational shift affects everything from daily transaction processing to long-term financial planning and regulatory compliance.

The introduction of AI into accounting is not about replacing human expertise. Instead, it provides powerful tools that handle high-volume, repetitive work with speed and consistency. This allows accountants and auditors to apply their skills to more complex problems, such as interpreting financial trends, assessing risk, and advising business leaders. For example, instead of spending days manually matching invoices to purchase orders, an accountant can use that time to analyze spending patterns and identify cost-saving opportunities. The technology helps teams work faster, produce more accurate reports, and manage compliance with greater confidence. The following sections explore three specific ways AI is reshaping accounting operations: automating data entry, improving financial reporting, and streamlining tax research. Each area shows how these tools can free up valuable time and resources for finance teams, turning the accounting function into a more strategic partner for the business.

Automate Data Entry and Transaction Processing

AI systems can take over many repetitive jobs in accounting. This includes tasks like processing expense reports, matching invoices, and recording transactions. Automating this work reduces the chance of human error and can speed up critical processes like the month-end close. According to research from Stanford, this automation allows accountants to focus on more strategic tasks. Instead of getting stuck on tedious data entry, professionals can use their time for analysis and problem-solving. This shift helps make their work more engaging and valuable to the company.

Improve Financial Reporting and Analysis

AI tools can analyze large volumes of financial data much faster than a human can. They are skilled at finding unusual transactions and identifying patterns that might signal risk. This capability is especially useful for auditors, who can use AI to help plan their work and focus on high-risk areas. The technology also provides more detailed data analysis, which makes financial reports more informative. With AI, organizations can move from static, historical reporting to more dynamic, real-time insights. This allows leaders to make informed decisions based on the most current information available.

Streamline Tax Research and Compliance

Tax research can be a time-consuming process. AI helps professionals find accurate answers from large volumes of tax information quickly. This efficiency allows accountants to spend less time searching for rules and more time focusing on compliance strategy and advising clients. By automating repetitive tasks like data entry and expense tracking, AI frees up accountants for higher-value work. This includes interpreting complex tax codes and developing strategies to optimize tax positions. This shift allows tax professionals to engage in activities that require critical thinking and deep expertise.

How AI Changes Audit Practices

Artificial intelligence is reshaping the audit profession. It moves the practice from a periodic, sample-based review to a more continuous and comprehensive analysis. Instead of testing a small fraction of transactions, auditors can now examine entire datasets. This shift allows teams to identify risks and control weaknesses much faster, providing a more accurate view of an organization's health. The ability to analyze 100% of a population of data, rather than a sample, fundamentally changes the level of assurance an audit can provide.

This change also redefines the auditor's role. With AI handling repetitive data processing, auditors can dedicate more time to judgment-based tasks. They can focus on investigating complex anomalies, advising on risk mitigation, and providing strategic insights to business leaders. According to research in the Journal of Accountancy, AI helps make audits better by quickly analyzing client information and spotting risks. This transition elevates the audit function from a compliance check to a source of strategic value for the organization. The focus moves from "did we follow the process?" to "is the process effective and are we managing the right risks?" This deeper level of inquiry is possible because technology handles the foundational work of data verification and organization, freeing up human expertise for more complex problem-solving.

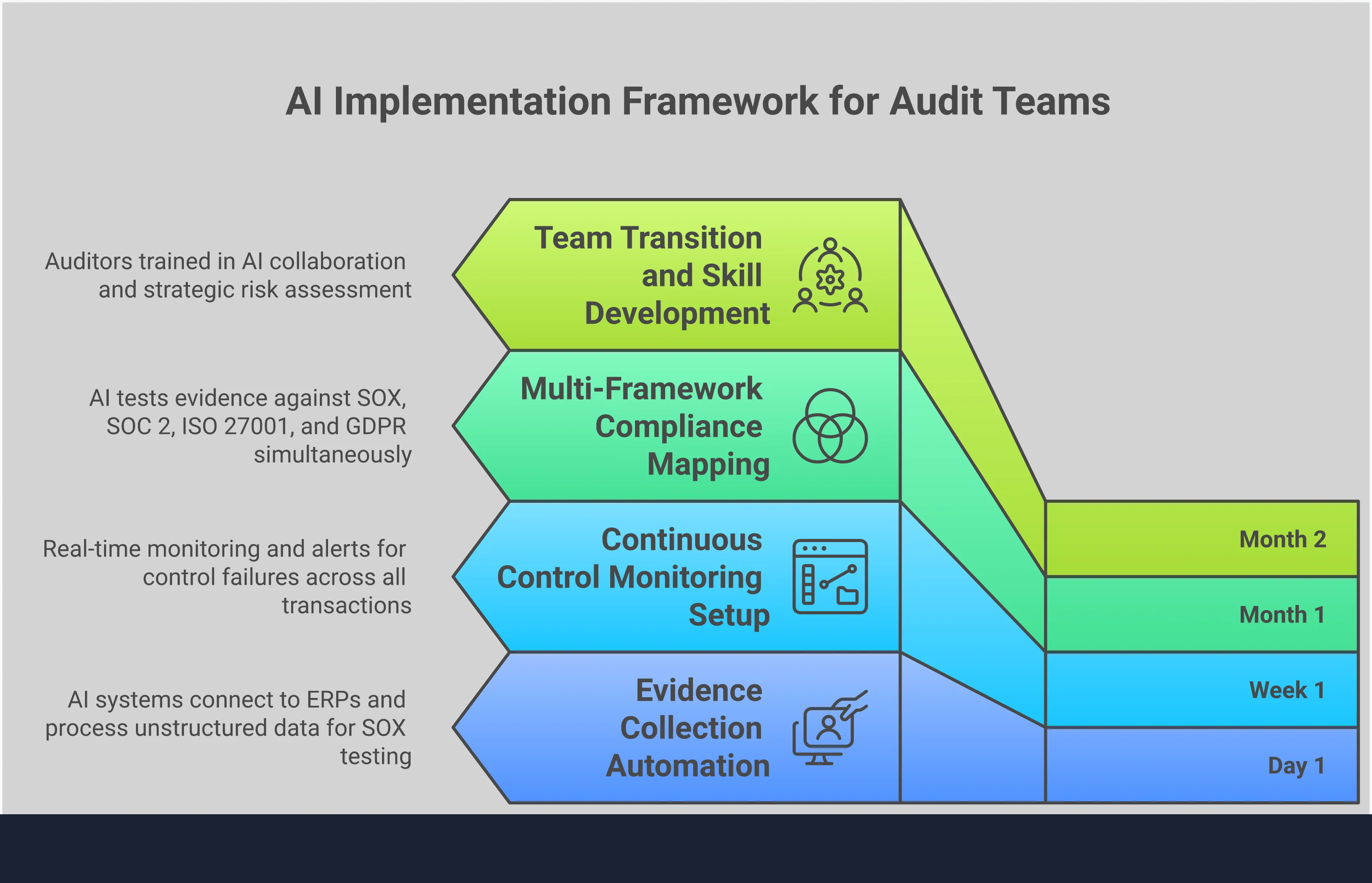

Automate Evidence Collection and Document Review

One of the most time-consuming parts of an audit is gathering and reviewing evidence. AI platforms automate this entire workflow. These tools can connect to different systems, pull relevant data, and compare it against control requirements. They can identify missing documents or inconsistent information without manual intervention.

This automation is especially useful for handling complex evidence types. AI can interpret unstructured data from messy PDFs, spreadsheets, and system screenshots. As noted by compliance experts at Strike Graph, generative AI is accelerating internal audits by automating tasks that previously took hours or days. This frees auditors from tedious document management, allowing them to focus on analysis and exceptions.

Improve Risk Assessment and Fraud Detection

AI significantly improves an auditor's ability to identify potential risks and fraudulent activities. Machine learning algorithms can analyze vast amounts of transactional data to find unusual patterns and outliers. These are anomalies that a human auditor, using traditional sampling methods, might easily miss.

By processing complete datasets, AI provides a more accurate picture of an organization's risk landscape. This capability allows audit teams to plan their work more effectively, focusing their attention on high-risk areas. The ability to detect fraud earlier and with greater precision helps protect the organization's assets and reputation. It transforms risk assessment from a static exercise into a dynamic, data-driven process.

Enable Continuous Monitoring and Real-Time Audits

Traditionally, audits happen at specific points in time, like the end of a quarter or year. This approach means control failures might go undetected for months. AI enables a shift toward continuous monitoring and real-time auditing. Systems can be configured to check controls and transactions as they occur.

This provides an up-to-the-minute view of the company's compliance posture. As BDO experts point out, AI is a tool that creates efficiencies, enabling auditors to spend more time on tasks requiring their specialized expertise. When a control fails or an unusual transaction is flagged, the system can alert the audit team immediately. This allows for prompt investigation and remediation, strengthening the overall control environment and ensuring the organization is always prepared for an audit.

What Are the Benefits of AI Integration?

Integrating artificial intelligence (AI) into accounting and auditing brings practical benefits to teams and organizations. By automating routine work, these systems help professionals focus on tasks that require human judgment and strategic thinking. The main advantages fall into three key areas: greater efficiency, improved accuracy, and better use of resources. This shift helps firms manage compliance workloads more effectively and deliver higher-value services.

Increase Efficiency and Productivity

One of the most immediate benefits of artificial intelligence is its ability to handle time-consuming tasks. This frees up your team for more complex work. AI systems can process expense reports, match invoices, and record transactions, which can speed up month-end closes significantly.

This shift allows accountants and auditors to spend less time on simple tasks and more on important advisory work. According to research from Stanford, AI is reshaping accounting jobs by taking on the more repetitive parts of the role. This allows skilled professionals to apply their expertise to analysis, strategy, and client relationships.

Improve Accuracy and Reduce Human Error

Automation helps reduce the risk of human error in repetitive financial tasks. Unlike people, AI systems perform calculations and data reviews with consistent precision. This is critical for maintaining compliance and ensuring the integrity of financial reporting.

Artificial intelligence can process huge amounts of information, like bank statements and contracts, much faster and with fewer mistakes than people can. The Journal of Accountancy notes that AI can help auditors by quickly analyzing large datasets to identify anomalies that might otherwise be missed. This leads to more reliable findings and a stronger compliance posture.

Reduce Costs and Optimize Resources

By improving efficiency and accuracy, artificial intelligence helps organizations reduce costs and make better use of their resources. When auditors can focus their time on the most important areas, they work more effectively and avoid wasting effort on less critical tasks.

This optimization allows firms to deliver deeper insights and better client service without increasing headcount. As The CPA Journal explains, firms that adopt AI can operate more efficiently, which translates into a competitive advantage. This allows you to reallocate budget and talent from manual review to strategic initiatives that drive business value.

Common Challenges of AI Implementation

Adopting artificial intelligence (AI) in accounting and audit is not a simple plug-and-play process. While the benefits are clear, implementation comes with its own set of challenges. These hurdles are not reasons to avoid AI, but they are critical factors to address for a successful transition. Firms that proactively manage these issues are better positioned to realize the full value of their technology investments.

Organizations must consider everything from the quality of their data to the skills of their people. Integrating new AI platforms with existing systems requires careful planning. And all of this must happen within a complex web of regulatory and ethical standards. Thinking through these issues beforehand helps ensure your AI initiative delivers on its potential to improve efficiency and accuracy. It turns a complex project into a manageable one with a clear path forward. The following sections explore four of the most common challenges and offer a framework for addressing them.

Address Data Quality and Security

Artificial intelligence models are only as effective as the data they learn from. If your data is inconsistent, incomplete, or inaccurate, the AI’s output will be unreliable. This makes data governance a foundational step. Before implementing an AI solution, your organization needs clean, structured, and secure data sets.

According to Mainstream Technologies, a key compliance issue is ensuring that AI-generated financial information is both transparent and auditable. AI tools used for financial analysis must meet the same high standards for accuracy and documentation as any manual process. This means your data security protocols must also extend to your AI systems, protecting sensitive information from unauthorized access and ensuring its integrity throughout the entire workflow.

Overcome Skill Gaps and Training Needs

AI is a tool that works alongside professionals, not in place of them. Its purpose is to handle repetitive tasks so auditors and accountants can focus on work that requires their specialized expertise. However, this shift requires new skills. Your team needs to understand how to use AI tools effectively, interpret their findings, and oversee their operations.

This creates a need for focused training and professional development. According to a report from BDO, AI should be used to augment human skills and create efficiencies. Employees must learn to collaborate with AI systems, moving from manual data processors to strategic analysts who can question, validate, and apply the insights that AI provides. This transition is essential for getting the most value from your technology investment.

Manage Integration with Existing Systems

New AI tools must fit into your existing technology stack. Many firms already use governance, risk, and compliance (GRC) platforms or enterprise resource planning (ERP) systems. An AI solution that cannot integrate with these systems will create data silos and inefficient workflows, defeating its purpose.

Beyond technical compatibility, a significant challenge is the need for transparency. Research published in the International Journal of Accounting Information Systems highlights that explainability is a major hurdle in AI adoption. If an AI system flags a transaction as high-risk, auditors must be able to understand and explain the reasoning behind that conclusion. This makes the "black box" problem a serious concern for audit and compliance teams who need to defend their findings.

Meet Regulatory and Ethical Requirements

The use of AI in finance is subject to growing scrutiny from regulators. Frameworks like the EU’s Artificial Intelligence Act establish specific requirements for high-risk AI systems, including those used in accounting. These regulations often mandate human oversight to ensure that automated decisions are fair, transparent, and accountable.

Adopting AI ethically means building trust into your systems. Your organization must be able to demonstrate how its AI models work and prove that they are free from bias. This involves creating clear documentation, establishing oversight procedures, and ensuring that every AI-driven conclusion is traceable and defensible. As Satva Solutions points out, embedding trust and accountability into your workflows is not just good practice; it is a core compliance requirement.

How AI Improves Compliance Automation

Artificial intelligence (AI) helps compliance and audit teams shift from periodic, sample-based testing to continuous, comprehensive monitoring. Instead of reacting to issues found during an audit cycle, organizations can use AI to identify and address compliance gaps as they happen. This approach helps teams manage risk more effectively and maintain a constant state of audit readiness.

AI platforms automate many of the repetitive parts of compliance work. This includes gathering evidence, reviewing documents, and testing controls against specific requirements. By handling these mechanical tasks, AI allows skilled professionals to focus on strategic analysis, risk assessment, and judgment. This shift improves efficiency and makes compliance roles more valuable to the organization.

Monitor Regulatory Changes in Real Time

Keeping up with changing regulations is a major challenge for compliance teams. AI systems can automatically track updates from regulatory bodies and news sources. This provides real-time alerts on new or modified requirements that could impact the organization.

This capability helps firms stay compliant with evolving rules without dedicating hours to manual research. According to Mainstream Technologies, real-time monitoring allows firms to adapt quickly and enhances their ability to build trust with clients and regulators. Instead of discovering a new requirement during an audit, teams can proactively adjust their controls and processes.

Automate Evidence Management and Audit Trails

A significant portion of any audit involves collecting, organizing, and reviewing evidence. AI can automate this entire workflow. These tools can connect to different business systems, pull relevant data, and compare it to control requirements. This process quickly identifies missing information or inconsistencies that would take a human auditor hours to find.

This automation creates a complete and traceable audit trail for every action. Every conclusion is linked directly back to the specific evidence evaluated and the testing procedure applied. This is critical for demonstrating compliance for frameworks like the Sarbanes-Oxley Act (SOX). It provides clear, defensible rationale for every finding, which simplifies reviews by external auditors.

Prevent Bias and Meet Transparency Requirements

As organizations use AI in more business functions, ensuring the fairness of those systems becomes a compliance issue. AI models used for compliance must be free from bias, and their decision-making processes must be explainable. This is essential for meeting ethical standards and regulatory expectations.

Firms must be able to demonstrate how an AI system reached a specific conclusion. This requires active monitoring to ensure that AI-generated data is auditable and that its decisions are fair. Maintaining this level of transparency is key to building trust in automated compliance systems and satisfying scrutiny from auditors and regulators.

Support Multiple Compliance Frameworks

Most organizations must comply with more than one regulatory framework, such as SOX, SOC 2, and ISO 27001. Manually mapping controls and evidence to each framework is redundant and inefficient. AI platforms can solve this by managing multiple compliance standards in a single system.

An AI tool can evaluate one piece of evidence and determine how it applies to several different controls across various frameworks. This "test once, comply many" approach saves time and ensures consistency. Guidance like the Artificial Intelligence Auditing Framework from The Institute of Internal Auditors (IIA) helps auditors assess these complex systems and their related risks.

AI Tools and Technologies in Use Today

Several types of artificial intelligence are already at work in accounting and auditing. These technologies are not a single, all-knowing system. Instead, they are a collection of specialized tools designed for specific tasks. Each tool helps professionals handle data, documents, and decisions with greater speed and accuracy. By understanding what each technology does, organizations can apply them to their most pressing challenges in compliance and financial reporting.

Firms are using artificial intelligence to automate routine work and gain deeper insights from financial information. Key technologies include generative AI, which can create summaries and analyze evidence, and Robotic Process Automation (RPA), which handles repetitive, rule-based tasks. They also use Natural Language Processing (NLP) to understand documents and machine learning to find hidden patterns in data. These tools often work together to support human judgment, not replace it. They manage the mechanical layers of compliance and audit work, allowing skilled professionals to focus on strategic analysis, complex exceptions, and the critical thinking that drives value. This shift helps teams move from reactive checking to proactive risk management.

Using Generative AI for Evidence

Generative artificial intelligence is changing how audit teams handle evidence. This technology can process large volumes of information, such as system reports and screenshots, and then generate clear, concise summaries. Instead of manually reviewing every document, auditors can use AI agents to perform the initial assessment, helping them quickly identify what is important.

According to research from Strike Graph, "Generative AI is accelerating internal compliance audits by automating tasks that previously took hours or even days." The technology can pull data from different systems, check it against control requirements, and flag any gaps. This automation allows auditors to focus their attention on resolving exceptions and assessing complex issues, making the entire audit process more efficient.

Using RPA for Repetitive Tasks

Robotic Process Automation (RPA) is designed to handle high-volume, repeatable tasks that do not require human judgment. Think of it as a digital assistant that can perform structured activities like data entry, invoice processing, and account reconciliations. RPA follows a set of pre-defined rules to complete tasks exactly as a person would, but much faster and without fatigue or error.

The main benefit of RPA is that it frees up skilled professionals from tedious work. As BDO Insights notes, artificial intelligence is a tool used to augment human skills and create efficiencies. This allows auditors and accountants to spend more time on strategic analysis, risk assessment, and client communication, where their expertise adds the most value.

Using NLP for Document Analysis

Natural Language Processing (NLP) gives computers the ability to read and interpret human language. This is especially useful in accounting and auditing, where professionals must review dense documents like contracts, leases, and regulatory filings. NLP can extract key terms, dates, and clauses from unstructured text, saving hundreds of hours of manual review.

This technology helps auditors make sense of complex information quickly. For example, The CPA Journal explains that artificial intelligence can read and understand long documents like new accounting standards. It can also scan financial reports to assess a company's health. By turning unstructured text into structured data, NLP makes document analysis faster and more consistent across the entire audit team.

Using Machine Learning for Anomaly Detection

Machine learning models analyze vast datasets to find patterns and predict outcomes. In an audit context, this technology is excellent at identifying anomalies that could signal fraud or control failures. A machine learning system can sift through millions of transactions to flag unusual activity that a human reviewer might easily miss using traditional sampling methods.

This capability makes audits more effective and risk-focused. According to the Journal of Accountancy, artificial intelligence helps auditors by "finding unusual transactions and patterns in large amounts of data." It can also help teams plan their audits and identify risks more accurately from the start. This allows auditors to concentrate their efforts on the areas of highest concern, leading to a more thorough examination.

How AI Will Change Professional Roles

The integration of artificial intelligence (AI) is not about replacing professionals in accounting and auditing. Instead, it is reshaping their roles and responsibilities. As AI systems handle more of the repetitive, data-intensive work, human experts are freed to concentrate on tasks that require critical thinking, judgment, and strategic insight. This evolution changes the day-to-day work of auditors and compliance officers, moving them from data processors to strategic advisors. The focus shifts toward interpreting complex information, managing new types of risk, and collaborating with technology to deliver greater value.

Shift from Manual Tasks to Strategic Advisory

Many professionals wonder how artificial intelligence will affect their jobs. The immediate impact is the automation of tedious work. AI can help with tasks like summarizing long documents and checking data for completeness, which have historically consumed a significant portion of an auditor's time. This shift allows professionals to move away from mechanical processes and toward higher-value activities. According to Thomson Reuters, AI helps accountants spend less time on simple tasks and more time on important advisory work. By handling the manual effort, AI enables auditors and accountants to focus on analysis, strategic planning, and building stronger client relationships.

New Skills Required for Compliance Officers

As AI becomes more common in business operations, compliance and audit professionals need new skills to provide effective oversight. Their role is expanding to include the governance of AI systems themselves. Professionals must now understand how these systems work, the data they use, and the potential risks they introduce, such as bias or error. The Institute of Internal Auditors (IIA) developed an Artificial Intelligence Auditing Framework to help internal auditors identify and manage these risks. This requires a focus on AI ethics, which involves embedding trust, transparency, and accountability into automated systems and workflows to ensure they operate as intended.

Develop Human-AI Collaboration Models

The future of audit and compliance involves a partnership between humans and machines. AI is a tool that augments human skills, creating efficiencies that let auditors focus on tasks requiring their specialized expertise. In this collaborative model, AI handles the large-scale data analysis, while humans provide context, exercise professional skepticism, and make final judgments. As organizations adopt AI, the internal audit team plays a key role in addressing the associated risks. According to Grant Thornton, internal audit can be fundamental for AI success by helping the organization manage risks before they become problems. This partnership allows teams to deliver more thorough and insightful audits.

The Future of AI in Accounting and Auditing

Artificial intelligence (AI) is reshaping the fields of accounting and auditing. It helps professionals move beyond repetitive tasks and focus on strategic analysis. As these technologies become more integrated into daily workflows, they will change how organizations manage compliance, assess risk, and conduct audits. The future points toward a partnership where human expertise guides AI-driven tools to produce faster, more reliable financial oversight.

Key Trends and Future Technologies

Firms are adopting automation and predictive analytics to improve how they operate and serve clients. The goal is not to replace human judgment but to support it. According to BDO, AI is a tool used to augment human skills and create efficiencies. This allows auditors to spend more time on complex tasks that require their specialized knowledge. Future developments will likely focus on making AI systems more intuitive and capable of handling increasingly complex financial scenarios, from forecasting to real-time risk modeling.

The Shift to Continuous Auditing

The move away from periodic, backward-looking audits toward continuous monitoring is a significant trend. Generative AI is speeding up internal compliance audits by automating tasks that once required days of manual work. This allows for real-time evaluation of controls and transactions. As Grant Thornton notes, internal audit teams play a key role in helping organizations understand how AI is used, ensuring security and compliance. This shift enables companies to maintain a state of continuous audit readiness, identifying and addressing issues as they happen instead of months later.

Long-Term Impact on Professional Standards

The integration of AI introduces new ethical and regulatory considerations. According to research published in ScienceDirect, key challenges include ensuring transparency and explainability, managing potential bias, and protecting data privacy. To maintain trust, firms must build accountability into their AI systems. This means creating clear audit trails that show how a conclusion was reached. Professional standards will evolve to require that AI-driven decisions are fair, defensible, and aligned with established ethical guidelines, placing a greater emphasis on the governance of these systems.

How to Prepare Your Organization for AI

Adopting artificial intelligence (AI) is not just a technical project. It requires careful planning, evaluation, and a commitment to helping your team adapt. A thoughtful approach ensures you select the right tools and build a foundation for long-term success. By focusing on strategy, technology, and people, you can integrate AI into your accounting and audit functions smoothly.

Build an Implementation Strategy

A successful AI adoption starts with a clear plan. Before you review any software, your organization should define what it wants to achieve. This strategy should involve leaders from audit, compliance, and IT.

Internal audit teams play a key role. They can help the organization identify and address risks before a new system is in place. This proactive approach helps ensure that any AI solution aligns with your company’s risk tolerance and compliance obligations from the very beginning. A good strategy sets clear goals, defines success metrics, and outlines how the technology will fit into existing workflows.

Evaluate AI Solutions for Your Firm

Not all AI tools are created equal. When evaluating solutions, look beyond features and focus on core requirements for audit and compliance. The system’s outputs must be transparent, explainable, and auditable.

Ask vendors how their platform ensures accuracy and documents its processes. AI-generated financial data must meet the same documentation and security standards as your manual work. You should be able to trace every conclusion back to the source evidence. This ensures that your team can defend its findings to regulators, external auditors, and leadership. Choose a solution that provides a clear audit trail for every action.

Manage Change and Plan for Training

Introducing AI changes how your team works. It is important to manage this transition with clear communication and training. The goal is to show how AI can help professionals focus on more strategic work, not replace them.

Training should focus on how AI can augment human skills, freeing up auditors and accountants for tasks that require critical judgment. Adopting AI is also a cultural shift. It requires building trust in the new systems. You can foster this trust by being transparent about how the technology works and by creating accountability for its use in your daily workflows.

Related Articles

FAQs: AI in Accounting and Auditing

Table of Contents

Mike Reeves, PhD

Mike is a key figure at the intersection of psychology and technology. He has created and managed algorithms and decision-making tools used by more than half of the Fortune 100.