Article

What Is Accounting Automation & How It Works

Eric Sydell, PhD

|

Updated on

|

Created on

For public companies, maintaining compliance with regulations like the Sarbanes-Oxley Act (SOX) is a critical, high-pressure responsibility. The process often involves a stressful, last-minute rush to gather evidence and test hundreds of internal controls. Manual testing and evidence review are slow and introduce the risk of human error, creating potential gaps in your audit trail and leaving your organization vulnerable. Accounting automation strengthens compliance by creating consistent, repeatable workflows for financial processes. It builds a clear, defensible record for every transaction and control test. This approach helps organizations move from periodic spot-checks to a state of continuous audit readiness, making the audit process smoother for everyone involved.

Key Takeaways

Shift your team from manual tasks to strategic work: Automation handles repetitive processes like data entry and reconciliation, allowing skilled professionals to focus on financial analysis, risk assessment, and providing business insights.

Plan your implementation carefully: A successful transition involves more than just software. Prepare your team for new workflows, establish clear data quality standards, and maintain human oversight for critical decisions.

Strengthen compliance and measure your return: Automation produces consistent, defensible audit trails for easier audits. You can demonstrate its value by tracking metrics like lower error rates, faster financial closes, and direct cost savings.

What Is Accounting Automation?

Accounting automation uses software to perform financial tasks that people would otherwise handle manually. This includes routine work like data entry, processing invoices, and reconciling bank statements. The goal is not to replace accountants, but to equip them with tools that manage high-volume, repetitive work with greater speed and accuracy.

By connecting directly with financial systems and bank accounts, these tools create a central place for financial data, reducing the time spent gathering documents and correcting errors. Industry analysis shows that accounting automation can significantly speed up the process of closing the books. It gives finance teams access to real-time information, allowing them to move from simply recording data to analyzing it.

This shift is important for functions like internal audit and compliance. When routine tasks are automated, skilled professionals can focus on higher-value work, such as investigating anomalies, assessing risk, and providing strategic advice to business leaders. Automation provides the clean, reliable data needed to make those activities more effective. It helps turn the accounting function from a cost center into a source of valuable business insight.

The Technology Driving Automation

Several key technologies make accounting automation possible. Robotic Process Automation (RPA) uses software “bots” to mimic human actions for high-volume, rules-based tasks like entering data or processing payments. This approach is ideal for work that is repetitive and follows a clear set of steps.

Artificial intelligence (AI) and machine learning handle more complex jobs. These systems can learn to spot unusual transactions, categorize expenses automatically, and process documents that do not follow a standard format. Another important technology is Optical Character Recognition (OCR), which allows software to read and extract data from PDFs and scanned invoices, eliminating manual data entry.

How Automation Differs From Traditional Accounting

The biggest difference between automated and traditional accounting is the role of the accountant. In a traditional model, professionals spend a large portion of their time on manual data collection and entry. This work is essential but time-consuming and prone to human error.

Automation handles these repetitive tasks, freeing accountants to concentrate on more strategic work. Instead of just preparing reports, they can analyze financial data to identify trends and advise business leaders. This shift also strengthens compliance. By streamlining financial processes, automation minimizes errors and helps ensure the business adheres to regulations, reducing the risk of penalties. It allows teams to build a more consistent and defensible process.

How Does Accounting Automation Work?

Accounting automation software replaces manual, repetitive tasks with digital workflows. Instead of a person physically handling invoices, entering data into spreadsheets, or matching purchase orders, software does the work. The process generally follows three main steps: capturing data, applying rules to process it, and integrating the results with other financial systems.

Think of it as creating a digital assembly line for your financial information. Raw data, like a vendor invoice, enters at one end. The system automatically reads the document, understands its contents, and checks it for accuracy. It then routes the information for approvals and posts the final transaction to your accounting ledger, all guided by rules you define.

The goal is to create a consistent, repeatable process that reduces the need for human intervention in routine tasks. This allows finance and audit teams to spend less time on mechanical work and more time on analysis and strategic judgment. The entire workflow is designed to connect different accounting functions, creating a single, efficient system for managing financial data from start to finish. It streamlines processes by integrating various accounting tasks into one workflow, ensuring information moves smoothly from invoices to approvals and finally to financial reports.

Capturing and Processing Data

The first step in automation is getting information into the system without manual data entry. Automation software uses technology like optical character recognition (OCR) to read and extract key details from documents. This includes invoices, receipts, and bank statements. The tool can identify information such as vendor names, invoice numbers, dates, and line-item amounts.

Once the data is captured, the system processes it. It can digitize information from messy PDFs, spreadsheets, and other common file types. This eliminates the time-consuming and error-prone task of typing information by hand. The result is structured, digital data that is ready for the next stage of the automated workflow.

Applying Rules and AI

After data is captured, the software applies rules and Artificial Intelligence (AI) to handle it. These rules reflect your company’s internal processes. For example, you can set a rule to automatically route any invoice over $5,000 to a department head for approval. The system can also match purchase orders to invoices and receipts, flagging any discrepancies.

This is where automation moves beyond simple data entry. By using AI agents, the software can perform validation checks and make decisions based on the information it processes. It ensures that transactions are coded correctly and adhere to internal controls. This automated verification helps maintain accuracy and consistency across all financial operations.

Integrating with Financial Systems

The final step is to connect the automated workflow with your core financial systems. Automation tools are designed to integrate with your existing Enterprise Resource Planning (ERP) platform and general ledger. This ensures that all transactional data flows seamlessly into your official accounting records without needing to be re-entered.

This integration creates a unified and efficient workflow. When an invoice is approved, the transaction is automatically recorded in the correct accounts. This keeps your financial data current and accurate at all times. A well-integrated system provides a single source of truth for financial reporting, which is essential for maintaining compliance and preparing for audits.

What Are the Key Benefits of Accounting Automation?

Automating accounting tasks offers more than just speed. It introduces a new level of precision, cost-effectiveness, and control to financial operations. By handling repetitive work, these systems allow your team to focus on analysis and strategy. This shift helps organizations improve efficiency, reduce errors, and strengthen their financial governance. The benefits extend from daily bookkeeping to year-end audits, creating a more resilient and transparent financial environment.

Save Time and Improve Efficiency

Manual accounting tasks like data entry, reconciliation, and report generation are time-consuming. Automation takes over these repetitive processes, running them faster and more consistently than any human could. According to research from FinOptimal, accounting automation can "significantly streamline various financial processes, allowing small businesses to focus on growth." This frees up your skilled finance professionals from tedious work. Instead of chasing down invoices or matching receipts, they can spend their time on financial analysis, strategic planning, and advising business leaders. This reallocation of human expertise is where the greatest efficiency gains are found.

Increase Accuracy and Reduce Errors

Even the most careful person can make mistakes. Manual data entry is a common source of errors that can lead to incorrect financial statements and poor business decisions. Automation minimizes this risk by applying predefined rules and logic to every transaction. Systems can validate data as it enters, flag inconsistencies, and ensure calculations are correct every time. This consistency is crucial for compliance. As FinOptimal notes, "Streamlining processes minimizes errors and ensures adherence to relevant regulations, reducing the risk of penalties." By reducing human error, you create more reliable financial reports and a stronger foundation for your business.

Lower Costs and See a Return on Investment

Automating accounting processes can lead to significant cost savings. It reduces the hours your team spends on manual tasks, which can lower overtime and labor costs. It also helps avoid the financial penalties that come from compliance errors or late filings. While there is an upfront investment in software and implementation, the return is often clear. According to Amerit Consulting, firms with strong accounting automation skills can deliver better service and find new opportunities. This makes automation a strategic investment that improves your bottom line through both direct savings and increased operational capacity.

Strengthen Compliance and Audit Readiness

For any company, especially those subject to regulations like the Sarbanes-Oxley Act (SOX), maintaining compliance is critical. Automation helps by creating clear, consistent, and easily accessible audit trails for every transaction. It ensures that controls are applied uniformly and that documentation is always in order. This approach transforms how businesses manage compliance, helping them "improve accuracy, streamline processes, and reduce risks." Instead of a stressful, last-minute rush to gather documents for an audit, your organization can maintain a state of continuous audit readiness. This makes the audit process smoother for both your team and external auditors.

Which Accounting Tasks Can You Automate?

Accounting automation is best applied to tasks that are repetitive, rule-based, and data-intensive. By handing these processes over to software, finance teams can shift their focus from manual data entry to strategic analysis and decision-making. Automation tools are designed to handle a wide range of functions, from daily transaction processing to month-end closing and financial reporting. The key is to identify the areas where manual work creates bottlenecks, consumes valuable time, or introduces the risk of error.

Many core accounting functions can be automated in part or in full. These include processing invoices, reconciling accounts, managing employee expenses, running payroll, and generating financial reports. The goal is not to replace accountants but to provide them with tools that handle the mechanical work. This allows them to apply their expertise to more complex issues like financial planning, risk management, and business strategy. As technology improves, the scope of what can be automated continues to expand, offering new ways to make finance departments more efficient and accurate.

Accounts Payable and Receivable

Managing accounts payable (AP) and accounts receivable (AR) involves a high volume of repetitive tasks. Automation can streamline these workflows significantly. For AP, software can automatically capture invoice data, match it to purchase orders, and route it through digital approval workflows. Once approved, the system can schedule payments to optimize cash flow.

For AR, automation helps generate and send invoices, track payment statuses, and send automated reminders for overdue accounts. This reduces the manual effort required to manage collections and improves the consistency of communication with customers. According to research from Tipalti, this level of accounting automation helps businesses manage their payables and receivables more efficiently, reducing errors and freeing up staff time.

General Ledger Reconciliation

Reconciling the general ledger is a critical step in the month-end closing process, but it is often tedious and prone to human error. Automation tools can speed up this process by automatically matching transactions between different accounts, such as bank statements and the general ledger. The software can quickly identify discrepancies that require manual investigation.

By automating the matching of thousands of transactions, companies can significantly accelerate their financial close. This not only saves time but also increases the accuracy of financial statements. Instead of spending days manually ticking and tying numbers, accountants can focus their attention on resolving the exceptions flagged by the system, leading to a more efficient and reliable reconciliation process.

Expense Management and Reporting

Handling employee expense claims is another area where automation delivers clear benefits. Instead of manual data entry and paper receipts, employees can use mobile apps to submit expenses on the go. AI-powered tools can then automatically pull important details like the vendor, date, and amount directly from a photo of a receipt.

The system can also check submissions against company expense policies in real time, flagging any out-of-policy spending for review. This simplifies the process for employees and ensures that claims are accurate and compliant before they are approved. For the finance team, this means less time spent chasing down receipts and correcting errors, and more time analyzing spending patterns.

Payroll and Tax Calculations

Payroll processing is a complex and high-stakes function where accuracy is essential. Automation tools can handle the entire process, from calculating wages and deductions to filing taxes and distributing payments. These systems stay up-to-date with changing tax regulations, which helps ensure compliance and reduces the risk of penalties.

By automating payroll, businesses can ensure their employees are paid accurately and on time, every time. According to Digits, using tools to automatically calculate wages and manage tax filings makes the entire process more efficient and reliable. This removes a significant administrative burden from the finance team and provides a clear, consistent process for managing compensation.

Financial Reporting and Analytics

Creating financial reports and analyzing performance are essential for strategic decision-making. Automation tools can connect to various financial systems to automatically gather data and generate standard reports, such as income statements, balance sheets, and cash flow statements. This eliminates the need for manual data consolidation in spreadsheets.

More advanced tools use AI to analyze financial data, identify trends, and flag unusual patterns that might indicate an error or a business opportunity. As the CPA Journal notes, this allows accountants to spend less time gathering information and more time on evaluating financial data. This shift from data collection to analysis allows the finance team to provide more valuable insights to business leaders.

How Automation Improves Compliance

Automate Control Testing and Evidence Review

Manual control testing is slow and prone to human error. Automation changes this by systematically evaluating evidence against control requirements. Instead of auditors manually checking hundreds of messy PDFs or spreadsheets, an automated system performs these checks consistently across thousands of documents. This approach helps automate control testing and evidence review, reducing mistakes and freeing up your team for higher-value work.

By streamlining these processes, you ensure your organization adheres to regulations more effectively. This enhanced accuracy minimizes the chance of compliance failures and potential penalties.

Monitor for Regulatory Adherence

Compliance is not a once-a-year event. Automation enables a shift from periodic spot-checks to continuous monitoring of your control environment. An automated system can run tests and flag exceptions in near real-time, giving you a current view of your compliance posture. This allows you to identify and address control weaknesses as they happen, not months later during an official audit.

This proactive approach helps you maintain adherence to standards day in and day out. It transforms compliance from a reactive, stressful exercise into a managed, ongoing business process.

Create and Maintain Clear Audit Trails

A strong compliance program depends on a clear, defensible record of activities. Automation tools create a complete digital audit trail for every transaction and control test. Every step, from data collection to the final conclusion, is logged and time-stamped. This traceability is critical when you need to demonstrate compliance to external auditors or regulators.

This detailed record links every finding directly back to the source evidence, providing a clear path for reviewers. This improvement in information quality also supports more informed strategic decisions. A reliable audit trail makes it easier to answer inquiries and prove the integrity of your financial reporting.

Support for SOX, GAAP, and Other Standards

Most organizations must comply with multiple regulatory frameworks. Automation platforms can be configured to test controls against various standards simultaneously. Whether you are managing requirements for the Sarbanes-Oxley Act (SOX), Generally Accepted Accounting Principles (GAAP), or ISO 27001, a single system can handle them all. This harmonizes your compliance efforts and ensures consistent application of rules.

This capability is valuable for companies operating in multiple regions. Instead of running separate audit programs, you can manage compliance from a central platform. This reduces redundant work and provides leadership with a unified view of risk, helping prevent errors in regulatory reports.

Common Challenges in Accounting Automation

While accounting automation offers clear benefits, the transition requires careful planning. Shifting from manual processes to automated systems introduces new variables that teams must manage. Organizations often face challenges related to data security, team adoption, system oversight, and information quality.

Addressing these potential issues is key to a successful implementation. By understanding the common hurdles, finance and audit leaders can create a strategy that prepares the team for change and ensures the new tools deliver on their intended value. The following sections explore these challenges in more detail.

Data Security and Protection

Automating accounting tasks involves handling sensitive financial information. This concentration of data creates a critical need for strong security measures. If not properly secured, automated systems can become a target for cyberattacks, putting financial records and customer information at risk.

According to research from Deloitte, errors in automation can also affect the accuracy of regulatory reports, which may lead to fines or other penalties. To mitigate these risks, organizations must choose platforms with enterprise-grade security controls, including data encryption and robust access management. Protecting sensitive data is fundamental to maintaining trust with regulators, auditors, and stakeholders.

Implementation and Team Adoption

Technology is only one part of the automation equation; people are the other. A common hurdle is employee resistance, which often stems from a lack of clarity about how automation will affect daily work. According to IntegraBalance, teams need to embrace a clearer vision to move forward successfully.

Without proper support, even the best tools can fail to gain traction. As SafeBooks notes, training and integration challenges can arise when first introducing automation into a workflow. Effective change management, clear communication about benefits, and hands-on training are essential for helping your team adapt and feel confident using new systems.

The Need for Human Oversight

Automation is designed to assist human experts, not replace their judgment. Relying entirely on automated systems without proper supervision can introduce new risks. As the team at Forms on Fire explains, the improper implementation or automation of the wrong processes can result in financial losses or data integrity issues.

Human oversight is critical for reviewing exceptions, validating system outputs, and handling complex scenarios that require nuanced judgment. An effective automation strategy includes a "human-in-the-loop" approach, where people are responsible for final approvals and strategic decisions. This balance ensures that the efficiency gains from automation do not come at the expense of accuracy and accountability.

Maintaining Data Quality

The effectiveness of any automation tool depends entirely on the quality of the data it uses. Inaccurate or inconsistent data will lead to flawed outputs, undermining the reliability of your financial reporting and analysis. This principle is often summarized as "garbage in, garbage out."

To achieve reliable results, you must establish and enforce data quality standards. As the experts at FinOptimal point out, "accurate data is essential for successful accounting automation." This involves implementing data validation rules, cleaning up existing records, and regularly auditing your financial information. High-quality data ensures that your automated systems produce trustworthy insights, which supports better-informed business decisions.

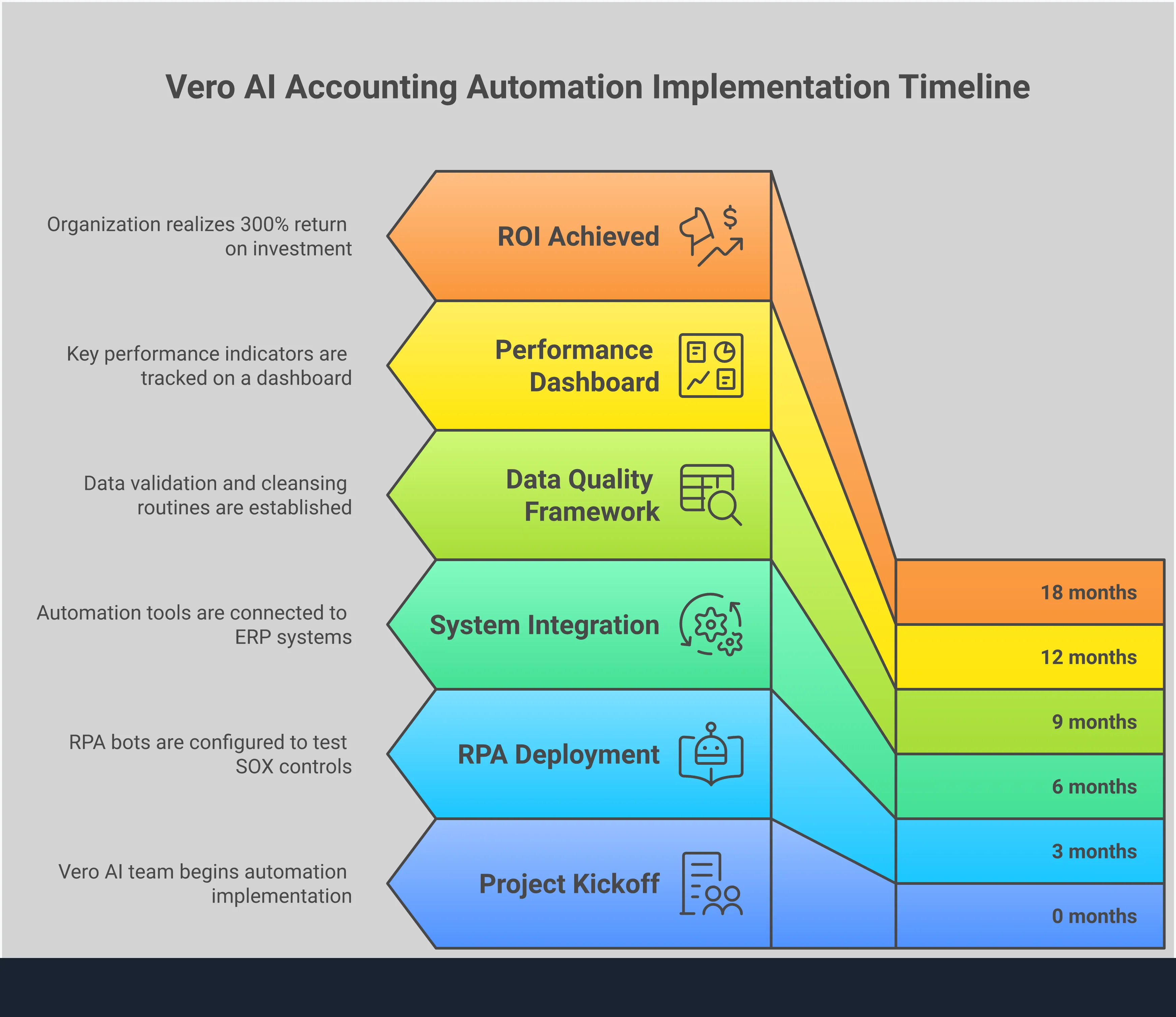

How to Overcome Implementation Challenges

Adopting new technology always comes with a learning curve. Accounting automation is no different. The most common hurdles are not technical but human. They involve managing change, ensuring data quality, and finding the right balance between machine efficiency and human expertise. Many organizations focus heavily on the software itself but overlook the foundational work required to make it successful. This can lead to low adoption rates, inaccurate results, and a failure to achieve the expected return on investment. Without a strategy for these challenges, even the most powerful tools can fall short.

A successful implementation requires a clear plan that addresses these areas from the start. This involves assessing your current workflows, identifying the specific processes you want to automate, and setting clear goals for what success looks like. By preparing your team, processes, and data, you can avoid common pitfalls and ensure the new system delivers on its potential. The goal is to create a smooth transition that builds confidence, minimizes disruption, and delivers value quickly. A thoughtful approach transforms a potentially difficult project into a strategic advantage for your finance and compliance teams, turning a simple software rollout into a true process improvement initiative.

Train Your Team and Manage Change

New tools require new skills and workflows. Without proper training and support, your team may resist the change or struggle to use the software effectively. It is important to communicate why the change is happening, focusing on how automation will reduce repetitive tasks and allow employees to focus on more strategic work.

Create a structured training program that covers the new system's features and how they fit into your team's daily responsibilities. As one report on auditing technology notes, training and integration challenges are manageable with an efficient and effective plan. Identify champions within your team who can help their peers and provide feedback. This approach helps build momentum and ensures everyone feels supported during the transition.

Set Data Validation and Quality Rules

Automation is only as reliable as the data it uses. Inaccurate or incomplete information can lead to flawed outputs and undermine trust in the system. Before you implement any new tool, you need to establish clear standards for data quality. This means cleaning up existing data and setting rules to ensure new data is entered correctly.

Implement data validation rules within your systems to catch errors at the source. According to financial experts, accurate data is essential for successful accounting automation. Regularly audit your financial information to maintain its integrity. This proactive approach ensures your automation tools produce reliable insights, which leads to better-informed decisions and a smoother audit process.

Balance Automation with Human Judgment

Automation should augment your team, not replace it. While software can handle repetitive, rule-based tasks with incredible speed and accuracy, it cannot replicate human judgment, critical thinking, or professional skepticism. Over-reliance on automation without proper oversight can introduce new risks, from financial misstatements to security vulnerabilities.

Define which processes are suitable for full automation and which require human review. As some experts warn, the improper implementation of automation can lead to significant errors. Use automation to flag exceptions and anomalies, then empower your team to investigate and resolve them. This combination of machine efficiency and human expertise creates a stronger, more resilient compliance and accounting function.

How to Choose the Right Automation Tools

Selecting the right automation software is a critical decision. The market offers many options, each with different strengths. A structured evaluation helps you find a tool that fits your team’s specific needs and supports your long-term goals. Focus on features, integration, and the ability to scale with your business.

Evaluate Essential Features

Start by identifying the core features your team needs. According to Intuit, it is important to look for tools with a user-friendly interface, customization options, and seamless integration. Most importantly, confirm the software has robust data security measures to protect sensitive financial information. Your tool should meet industry standards for encryption and access controls. This gives you confidence that your data is safe from unauthorized access. A clear security posture is non-negotiable for any financial tool, especially when handling information subject to audit and regulatory review.

Check for System Integration

Your automation tools should not create new data silos. The goal is to connect different accounting functions into a single, streamlined process. A well-integrated system connects bookkeeping, invoicing, payroll, and reporting. This creates a single source of truth for your financial data, which is essential for accurate reporting and smooth audits. Before choosing a tool, map out your existing systems, like your enterprise resource planning (ERP) software. Ensure any new software can connect with these systems through application programming interfaces (APIs) or pre-built connectors.

Consider Scalability and Customization

The tool you choose today should support your business tomorrow. As your company grows, your transaction volume and operational complexity will increase. Your software needs to handle this growth without slowing down. According to Tipalti, a scalable tool is one that can grow with your business. Also, consider how much you can customize the software. Every business has unique workflows and internal controls. A flexible tool allows you to configure rules and processes that match how your team works, rather than forcing you to adapt to a rigid, one-size-fits-all system.

What to Consider Before You Implement

A successful automation project starts with careful planning. Before you select a tool or begin implementation, it’s important to build a solid foundation. Taking the time to assess your current state, plan resources, and prepare your team will help ensure a smooth transition and better results.

Assess Your Current Processes

Before you can automate accounting tasks, you need a clear picture of your manual workflows. Documenting each step helps you identify the most repetitive, time-consuming, or error-prone areas that are prime candidates for automation. A clear process map provides a blueprint for your implementation.

Your data quality is just as important. Successful automation depends on accurate and reliable information. Before you begin, it’s wise to implement data validation rules and audit your financial records. Starting with clean data ensures that your automated processes produce trustworthy insights and support informed decisions.

Plan Your Budget and Timeline

Implementing automation requires a clear budget and a realistic timeline. Your current level of digitization will influence both. For example, teams that still rely on paper-based processes may need to account for extra time and resources to digitize documents before they can automate workflows.

Consider the full scope of the project, including software costs, implementation support, and team training. If your team feels overwhelmed by the process, you might explore managed services or seek expert advice from consultants. This can help you create a more accurate plan and ensure a smoother transition to an automated system.

Prepare Your Team for the Change

New technology often introduces training and integration challenges. Preparing your team is critical for adoption. Communicate a clear vision for how automation will support their work, not just change it. Frame the new tools as a way to remove tedious tasks and free them up for more strategic analysis.

Employee resistance can slow down or derail an implementation. You can overcome this by involving your team in the process early and providing comprehensive training. When employees understand the benefits and feel confident using the new system, they are more likely to embrace the change. Clear communication helps everyone align on the goals and work together toward a more efficient future.

How to Measure Automation Success

Implementing new technology is only the first step. To understand its true value, you need to measure its impact on your organization. Tracking the right metrics shows you where automation is working and helps you build a case for expanding its use. Success isn't just about speed; it's also about accuracy, compliance, and financial return. By establishing clear benchmarks before you begin, you can quantify the improvements and demonstrate the technology's contribution to your business goals.

Track Time and Efficiency Gains

One of the most direct ways to measure success is by tracking how much time your team saves. Manual accounting tasks are often repetitive and time-consuming. Automation handles these processes, freeing your team for more strategic work. Before you implement a new tool, benchmark how long it takes to complete key tasks like invoice processing or account reconciliation. After implementation, measure that same task again. You can also track metrics like the number of transactions processed per employee or the reduction in overtime hours. These figures provide clear evidence of financial automation's business impact and help justify the investment.

Measure Error Reduction and Accuracy

Human error is a natural part of manual data entry and processing. These small mistakes can lead to significant problems, from incorrect payments to flawed financial reports. Automation reduces this risk by applying consistent rules to every transaction. To measure this, track the rate of errors before and after you introduce automation. Look for a decrease in reconciliation discrepancies, duplicate payments, and other common mistakes. As one report on accounting automation pitfalls notes, accurate data is essential for reliable insights. A lower error rate not only improves the quality of your financial data but also builds trust in your reporting.

Monitor Compliance and Audit Readiness

Staying compliant with regulations like the Sarbanes-Oxley Act (SOX) is a major challenge for accounting teams. Automation helps by creating clear, consistent processes and maintaining detailed records. You can measure success by tracking the time it takes to prepare for an audit. A significant reduction indicates that your records are organized and accessible. Other key metrics include a decrease in audit findings or exceptions and the percentage of compliance tasks completed on time. Automation helps improve accounting compliance by minimizing manual errors and ensuring that processes adhere to required standards, which reduces the risk of penalties.

Calculate Cost Savings and ROI

Ultimately, any business investment needs to provide a positive return. Calculating the return on investment (ROI) for automation involves looking at both direct and indirect cost savings. Direct savings are easy to spot, including reduced labor costs from fewer manual hours, fewer late payment fees, and more early payment discounts captured. Indirect savings include lower external audit fees and the value of reallocating your team to higher-impact activities like financial analysis. You can also use specific compliance metrics to determine the cost-effectiveness of your program. This financial analysis provides a clear picture of how automation contributes to the bottom line.

Related Articles

Accounting Automation FAQs

Table of Contents

Eric Sydell, PhD

Eric has two decades of experience in enterprise technology and was a founder of Modern Hire, which became part of Hirevue in 2023.